Bitcoin-backed loans have quietly become one of the most flexible financial tools in the world. They allow Bitcoin holders to access liquidity without selling, without losing long-term upside, and without navigating traditional banking barriers.

But the real question most people have is not:

“What is a bitcoin-backed loan?”

It’s:

“How do people actually use bitcoin-backed loans, and how do I know if it’s right for me?”

This guide is built to help you think like a strategic Bitcoin borrower, with real-world stories, smart use cases, and the unique advantages only SALT clients have access to.

What we cover in this article:

- What is a Bitcoin-backed loan?

- Why borrow instead of selling Bitcoin?

- SALT’s 30/50/70 LTV Strategy Framework

- How Bitcoin-backed loans work (step-by-step)

- How SALT Shield™ protects you

- Stabilization explained

- The real-world use cases of bitcoin-backed loans

- Example SALT borrower profiles

- Multi-year vs short-term strategies

- Risks & considerations

- Common fears & misconceptions

- Who should and shouldn’t use a loan

1. What Is a Bitcoin-Backed Loan?

A Bitcoin-backed loan is a secured way to unlock liquidity without selling your Bitcoin. You use your BTC as collateral to borrow USD or stablecoins, while still keeping full exposure to Bitcoin’s long-term upside. There are no credit checks, no income documents, and no traditional bank underwriting. Your collateral, not your financial history, determines your approval. You get the cash you need when you need it, and you retain complete control over when and how you repay.

2. Why Borrow Instead of Selling Bitcoin?

Most of the time, people don’t borrow against Bitcoin because they “need a loan.” They actually borrow because they want access to liquidity without sacrificing their long-term position.

Here’s what a Bitcoin-backed loan helps you avoid:

Capital gains tax triggers (in many jurisdictions)

In many tax systems, selling Bitcoin is a taxable event. Borrowing, however, typically is not, meaning you can access cash without realizing a gain. (Always consult a tax professional; rules vary by region.)

Selling too early

Every long-term holder knows the pain of selling before the next run. Borrowing lets you keep exposure so you don’t miss out on future appreciation.

Selling during a dip

Market timing is brutal, even for professionals. A Bitcoin-backed loan gives you breathing room during downturns instead of forcing you to sell low.

Losing long-term upside

Bitcoin has historically rewarded patience. Borrowing lets you solve short-term needs while preserving your long-term thesis.

Traditional bank gatekeeping

Banks require:

- credit reports

- income verification

- employment history

- tax returns

- underwriting

- weeks of approvals

Crypto-backed loans bypass all of that. Your collateral, not your credit score, is what matters.

Slow, inflexible approval processes

Most borrowers are approved and funded within 48 business hours.. No committees. No interviews. No back-and-forth paperwork.

Bitcoin is a long-term asset yet life operates on short-term timelines. So borrowing against Bitcoin is how you bridge the two, accessing liquidity today while staying fully positioned for tomorrow.

3. SALT’s 30/50/70 LTV Framework: Which Borrower Are You?

Most competitors offer ~50% LTV and nothing more. SALT supports three distinct borrower archetypes, each with unique risk dynamics.

30% LTV: The Patient Builder

- Low volatility risk

- Most comfortable buffer

- Ideal for long-term Bitcoin believers

- Great for multi-year strategies

50% LTV: The Balanced Operator

- More liquidity

- Manageable if you understand volatility

- Good for business use cases and cash-flow planning

70% LTV: The High Gear Strategist

- Maximum liquidity

- Highest sensitivity to BTC price

- For experienced, active borrowers

Your LTV sets the tone for your entire borrowing plan.

4. How Bitcoin-Backed Loans Work (Step-by-Step)

Here is how bitcoin-backed loans work at SALT Lending:

- Deposit Bitcoin

BTC is transferred to secure collateral wallets. - Choose your LTV (30%, 50%, or 70%)

This determines your liquidity and risk buffer. - Receive USD or stablecoin

Funds arrive quickly. - Monitor LTV as markets move

LTV changes with the BTC price. - Enroll in SALT Shield™ or Stabilization if desired

These tools help protect your position during volatility. Eligibility requirements apply. - Repay when ready

No early repayment penalties. - Get your BTC back

Your full collateral is returned after payoff.

5. How SALT Shield™ Protects You

With SALT Shield™, there are no margin calls, no liquidations, no forced sell-offs, and zero market-triggered risk during the life of your loan. Your Bitcoin stays protected for the entire remaining term of your loan, regardless of volatility. To qualify, your loan must be over $50,000, have an LTV below 70%, and be at least three months from maturity.

Read more about SALT Shield™ here.

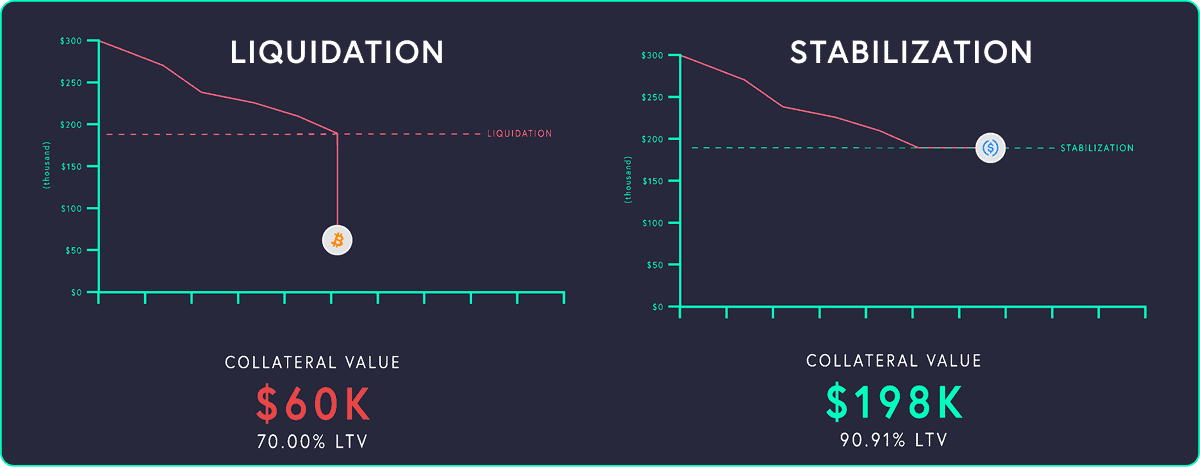

6. SALT Stabilization Explained Simply

Stabilization is SALT’s opt-in safety mechanism designed to protect your collateral during fast, unexpected market drops — without permanently closing out your loan.

Once you’ve opted in, Stabilization triggers automatically when your LTV reaches 90.91%. At that point, SALT converts your Bitcoin collateral into stablecoins, stopping further erosion in collateral value and giving your loan a chance to recover.

Think of it as a financial time-out: rather than a terminal event like liquidation — where your loan is closed and your Bitcoin is sold — Stabilization pauses the situation and holds your position steady.

From there, the path back is straightforward. To reactivate your loan, you bring your LTV to 83.33% or below through either a payment or a collateral deposit. Once that threshold is met, your stablecoins can be converted back to Bitcoin and your loan continues as normal.

Read more about Stabilization here.

7. Real-World Use Cases of Bitcoin-Backed Loans

PERSONAL USE CASES

Buying Real Estate

- Down payments

- Renovations

- Full cash purchases

- Rental acquisitions

For example:

A borrower in Florida uses a 30% LTV loan to secure a home deposit instead of selling BTC in a down market. They repay gradually while BTC recovers.

Funding Medical Expenses Without Selling

Life doesn’t wait for bull runs. Borrowing gives you stability without sacrificing long-term upside.

Education & Upskilling

Degrees, MBAs, bootcamps: borrowers use BTC-backed loans to fund future income while keeping their long-term holdings intact.

Debt Consolidation

Replacing high-interest debt with a BTC-backed loan is becoming mainstream, especially for freelancers and consultants with irregular income.

Lifestyle & Family Needs

Borrowers use these loans for:

- Weddings

- Home improvements

- Vehicles

- Travel

Especially when they’d rather not sell their long-term Bitcoin.

BUSINESS USE CASES

Business Expansion Without Dilution

Founders borrow for:

- hiring

- product development

- marketing

- new markets

- equipment

Without giving up equity or answering to banks.

Stabilizing Cash Flow (Freelancers + SMEs)

A small business uses BTC to bridge a seasonal revenue dip instead of taking expensive short-term credit.

Corporate Treasury Strategy

More companies today are treating Bitcoin not as a speculative experiment, but as a strategic balance-sheet asset. The playbook is simple:

Hold Bitcoin as a long-term treasury reserve, and use financing tools to unlock liquidity when needed.

Instead of selling their Bitcoin to fund operations, acquisitions, payroll, or expansion, companies borrow against their BTC. This allows them to:

- Preserve long-term exposure to an appreciating asset

- Free up operational capital without issuing equity or taking on traditional debt

- Reduce dilution for founders and shareholders

- Avoid selling during unfavorable market conditions

- Implement a disciplined, long-term treasury strategy

Some businesses use this approach to accumulate more Bitcoin, borrowing dollars at a known cost to increase their BTC holdings over time. Others use Bitcoin-backed loans to smooth cash flow, especially in industries where revenue is cyclical or seasonal.

Making Payroll in Crypto-Native Companies

Startups with BTC treasuries use BTC-backed loans to pay staff in periods of incoming revenue volatility.

INVESTMENT USE CASES

Buying More Bitcoin (Manual Leverage)

Borrow against your existing BTC to increase your position without selling what you already hold.

Diversifying Into Traditional Investments

Stocks, bonds, ETFs, and real estate, without selling BTC.

High-Level Trading Strategies (Hedging, Arbitrage, Cross-Market Moves)

Professionals use Bitcoin-backed liquidity to hedge options or execute neutral strategies while holding BTC long-term.

8. Example SALT Borrower Profiles

How Different People Use Bitcoin-Backed Loans

SALT’s borrowers span industries, ages, and financial backgrounds, but they share one thing in common: they want liquidity without giving up their Bitcoin. Here are three examples that illustrate how different needs, goals, and life stages shape how people use their BTC as collateral.

“The BTC Professional”: Age 32, United States

A mid-career analyst who has been dollar-cost averaging into Bitcoin since 2017. When a rental property opportunity appears, traditional financing falls through because his income is partly freelance. Instead of selling his BTC, triggering taxes and losing long-term upside, he uses a 30% LTV SALT loan to cover his down payment. After a refinance, he repays the loan in about 18 months, keeping both the property and his Bitcoin. For him, Bitcoin is his savings. Borrowing against it is how he upgrades his financial life without breaking his long-term thesis.

“The Crypto Founder”: Age 41, Europe

She runs a fast-growing Web3 startup and stores part of the company’s treasury in Bitcoin. Venture capital markets have tightened, and raising a bridge round would dilute the team. She takes a $300,000 loan at 50% LTV, using company BTC as collateral. This lets her make payroll, maintain runway, and keep operations moving, without selling treasury assets or issuing equity under pressure. For her, Bitcoin-backed borrowing isn’t just convenient; it’s a strategic corporate treasury tool that preserves ownership and protects employees.

“The Long-Term Holder”: Age 57, Middle East / EU

A decades-long investor who moved a portion of his retirement holdings into Bitcoin. Stability matters to him more than aggressive leverage. He upgrades his loan with SALT Shield™, protecting his 5 BTC from any margin calls or liquidation risk. He then borrows $120,000 to purchase a home abroad, confident that even major price swings won’t touch his collateral. For him, Shield™ isn’t a feature, it’s peace of mind.

9. Multi-Year vs Short-Term Strategies

Short-Term Loan Strategy (6–12 months)

- emergency liquidity

- quick opportunities

- income smoothing

Multi-Year Loan Strategy (1–3–5 years)

- property

- business expansion

- cash-flow smoothing

- BTC treasury strategy

- long-term conviction plans

SALT enables both paths.

10. Risks & Considerations

While Bitcoin-backed loans offer flexibility and powerful advantages, they also come with important risks every borrower should understand. Bitcoin’s price is volatile, which means your LTV can change quickly, especially during fast market swings. Higher LTVs bring borrowers closer to margin call and liquidation thresholds, unless they are protected by SALT Shield™, which removes market-triggered liquidation risk entirely during the life of a loan. Borrowers should also have a clear, realistic repayment plan, even if the loan offers flexible terms. These loans are most effective when used strategically, with a long-term mindset and responsible collateral management.

In summary, the risks and considerations of a bitcoin-backed loan are:

- Volatility

- LTV changes

- Liquidation risk (unless using Shield™

- Need for a repayment plan

11. Common Fears & Misconceptions Of Bitcoin-Backed Loans

“I’ll lose my Bitcoin.”

With SALT Shield™, you can eliminate margin call risk entirely during the life f the loan..

“Loans require credit checks.”

Not at SALT.

“Bitcoin loans are too expensive.”

Depends on:

- timing

- use case

- jurisdiction

- opportunity cost

For many borrowers, the upside retained outweighs interest cost.

“Platforms can fail.”

SALT maintains:

- strict licensing

- risk segregation

- Proven track record since 2016

- $0 in LENDER liquidity ever lost

12. Who Should and Shouldn’t Use a Bitcoin-Backed Loan?

Bitcoin-backed loans are powerful tools, but they’re not one-size-fits-all. They work exceptionally well for people who understand Bitcoin, value long-term holding, and want access to liquidity without selling their assets.

A Bitcoin-backed loan is best suited for:

- Long-term Bitcoin holders who want liquidity while keeping upside exposure

- Entrepreneurs and business owners who need flexible, fast capital without giving up equity

- Freelancers and self-employed earners who struggle with traditional bank underwriting

- Expats and globally mobile professionals who don’t want regional banking restrictions

- High-net-worth individuals using BTC strategically as part of a broader wealth plan

- People seeking to avoid taxable disposals in jurisdictions where loans are not taxable events

- Borrowers who value keeping their BTC stack intact while funding real-world needs

These borrowers tend to approach loans strategically, not emotionally, and understand how to manage collateral responsibly.

A Bitcoin-backed loan is not ideal for:

- Anyone without a liquidity buffer, savings, or access to emergency funds

- Borrowers taking 70% LTV with no prior experience managing crypto volatility

- People who panic during market swings and struggle to make calm, rational decisions

If you can’t tolerate volatility or have no plan for margin calls (unless using SALT Shield™), a crypto-backed loan may not be a fit.

Bitcoin-backed loans: Do you think it’s right for you?

The key takeaway is simple:

Bitcoin-backed loans aren’t about debt, they’re about strategy.

They allow you to keep the asset you believe in, maintain exposure to long-term appreciation, and still meet life’s opportunities and obligations. Whether you’re buying a home, funding a business, managing cash flow, or diversifying investments, a Bitcoin-backed loan can be the bridge between where you are today and where you want your wealth to go.

And with tools like SALT Shield™ and Stabilization, borrowers now have access to protections that simply don’t exist anywhere else in the industry. You can borrow confidently, knowing that volatility won’t derail your plans or jeopardize your long-term Bitcoin position.

In the end, Bitcoin-backed lending isn’t just about unlocking liquidity, it’s about unlocking freedom. Freedom from selling. Freedom from traditional banking barriers. And freedom to use your Bitcoin strategically, not reactively.

Ready to put your Bitcoin to work without selling it?