Ever wonder why we developed SALT Stabilization? Because we wanted our lending product to better align with our mission: to build products that increase access to financial opportunities and give people more control over their ability to generate long-term wealth.

Here’s the back story.

It all stemmed from the fact that Justin English — SALT’s chief executive officer– was a borrower with a SALT loan long before he became SALT’s CEO. Justin loved our loan product because it offered a way for people like him to get value out of his crypto assets without having to sell them. The only problem? Liquidation. After a single market crash Justin lost nearly 100% of his crypto portfolio. Having a deep understanding of the stress and pain that comes with constantly watching the market, Justin was well equipped and knowledgable when he stepped into the CEO role. He was able to take your feedback, combine it with his own experience and use it to improve our lending product.

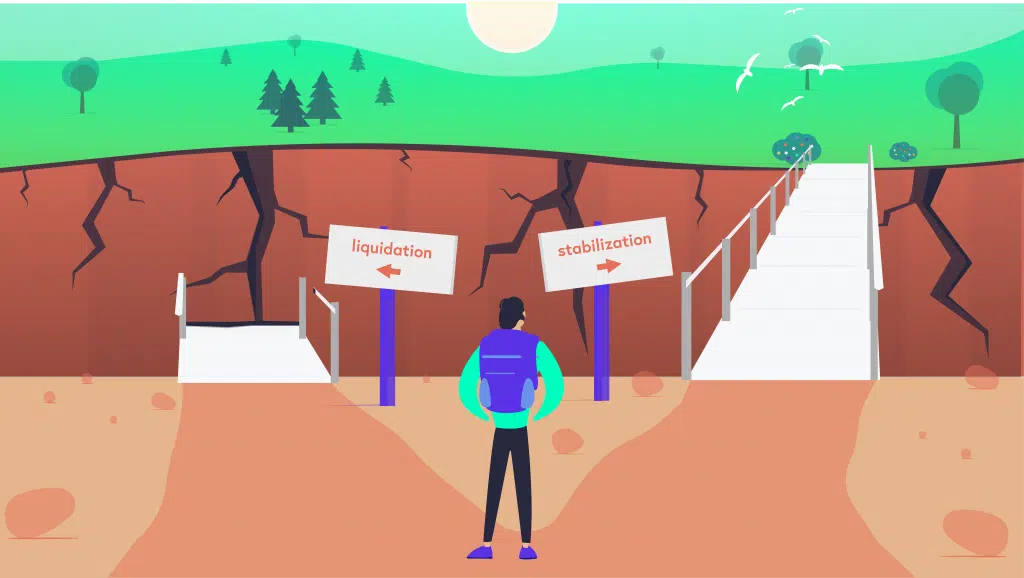

While our existing loan product was offering ways for our customers to escape some of the constraints of traditional finance, it wasn’t meeting the second part of our mission (helping people like you build long-term wealth) to the degree we wanted it to. While we know liquidation is a necessary part of crypto-backed lending, we also knew there had to be a better way to manage our clients’ loans during market crashes. We considered all the stress that comes with market volatility, and while we had (and still have) many tools in place to help you track the health of your loan (our Loan-to-Value Ratio monitor, real-time call, text and email notifications, etc.), we also realize that no matter how diligent you are about managing your loan, sometimes the market crashes faster than any of us can handle. Being a diligent borrower himself, Justin understood this pain point on a personal level and wanted to build a better product that could address and help alleviate some of the nail-biting stress that stems from constantly watching the market.

Introducing SALT Stabilization

Enter SALT Stabilization, the product designed to preserve wealth and reduce stress.

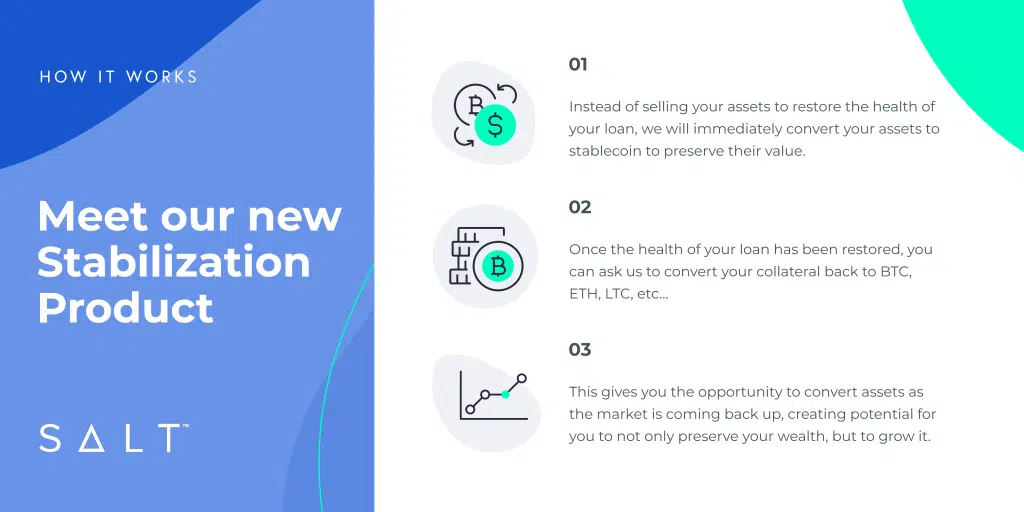

Instead of selling a portion of your crypto assets and using them to pay down your loan to restore it to a 70% LTV, with SALT Stabilization we convert your portfolio into stablecoin (USDC) once your loan-to-value ratio (LTV) hits our stabilization threshold of 90.91%. By doing so, we can offer you more control over how and when you want to restore the health of your loan. Once you cure your LTV back to a healthy level (below 83.33%), you are eligible to convert your portfolio back to the collateral mix of your choice when you’re ready.

Depending on how you time your conversion, you may even end up with more crypto assets than you had before you were stabilized. With SALT Stabilization, you can preserve the value of your crypto portfolio, and if you time it right, you can even grow it.

SALT Stabilization in Action

Since releasing SALT Stabilization in late 2020, we’ve had some time to see the product in action and learn more about how it preserves wealth for our clients during market volatility.

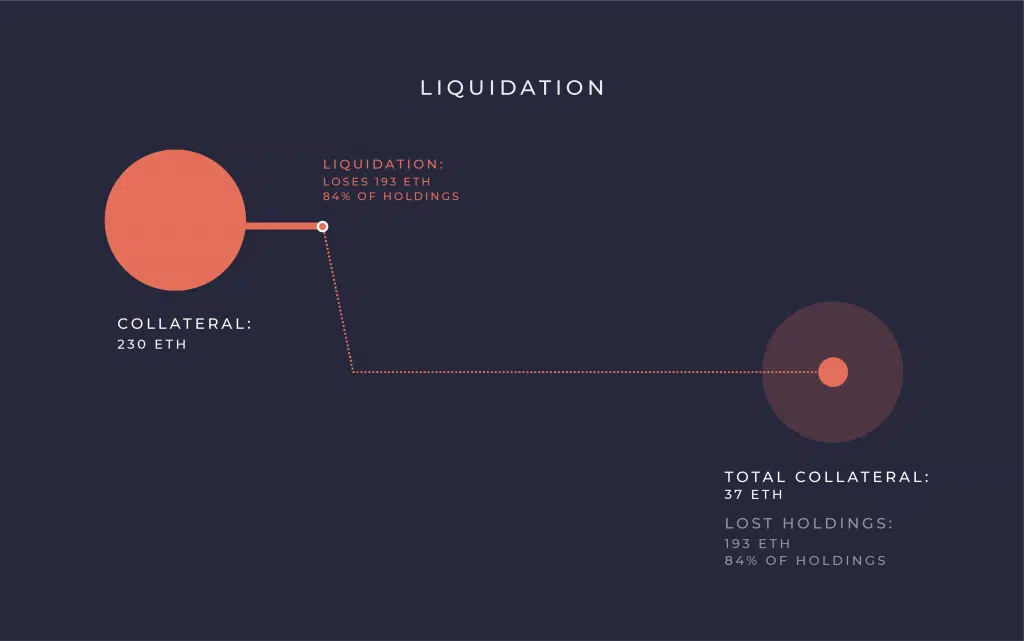

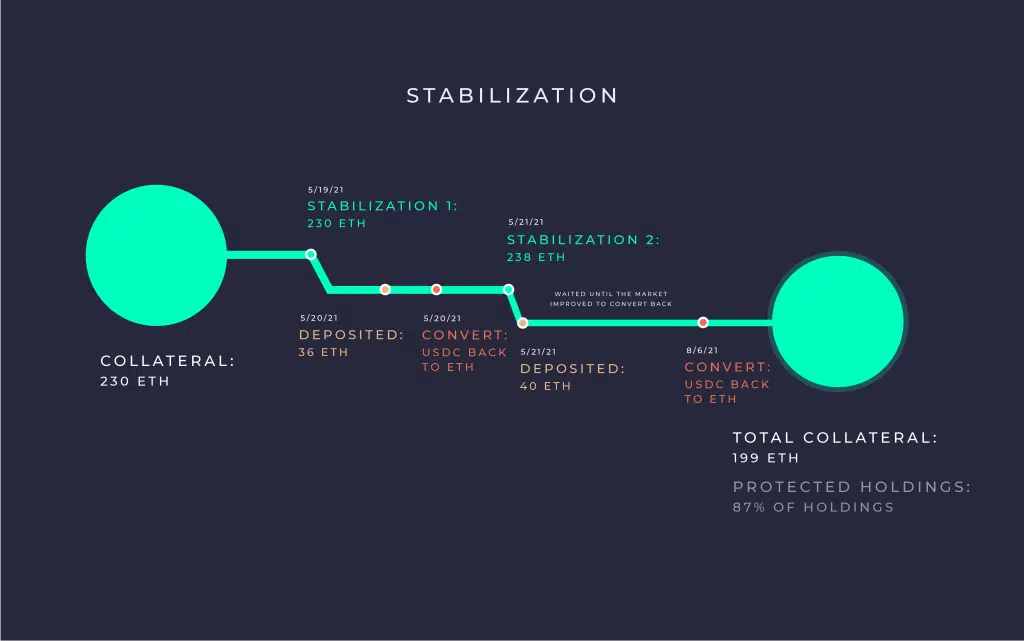

One of our customers experienced stabilization twice within a single week and converted the assets back both times. This particular customer converted his assets back fairly immediately following the first stabilization. However, following the second stabilization, he decided to wait, watch the market, and convert his assets back 80 days later. By offering him the option to leave his portfolio in stablecoin until he was ready to convert his assets back on his own terms, SALT Stabilization allowed the customer to preserve 87% of his portfolio. Had this same customer been liquidated twice under our previous model (the current model of other crypto lenders) he would only have 16% of his portfolio remaining following two liquidation events. This is a prime example of SALT Stabilization doing exactly what it was designed to do.

Old Method: Liquidation

New Method: SALT Stabilization

By having your portfolio converted to USDC during a market crash, you’re able to preserve the value of your portfolio to a degree that traditional liquidation would not allow.

If you’re on the fence about choosing a crypto-backed lender ask yourself:

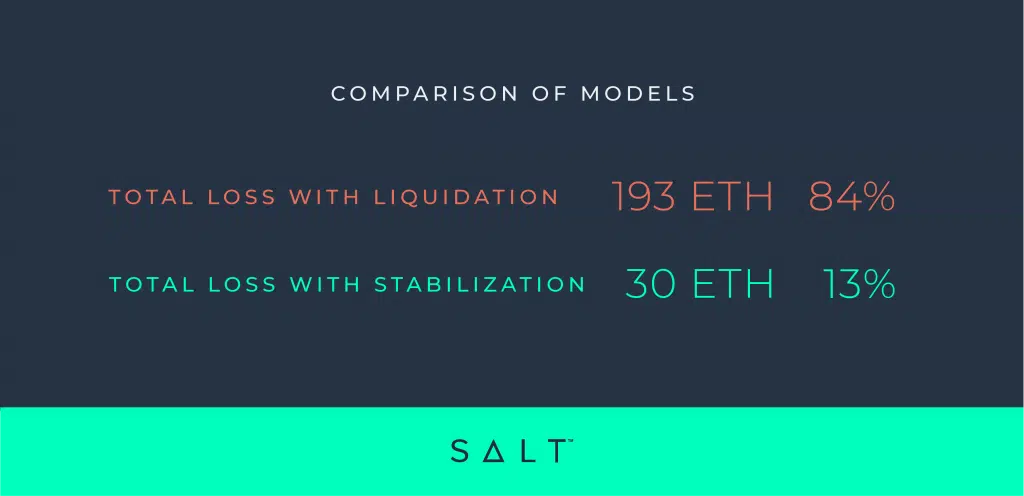

“When the market crashes would I rather lose 84% of my portfolio or 13%?

We’re pretty sure we know the answer.