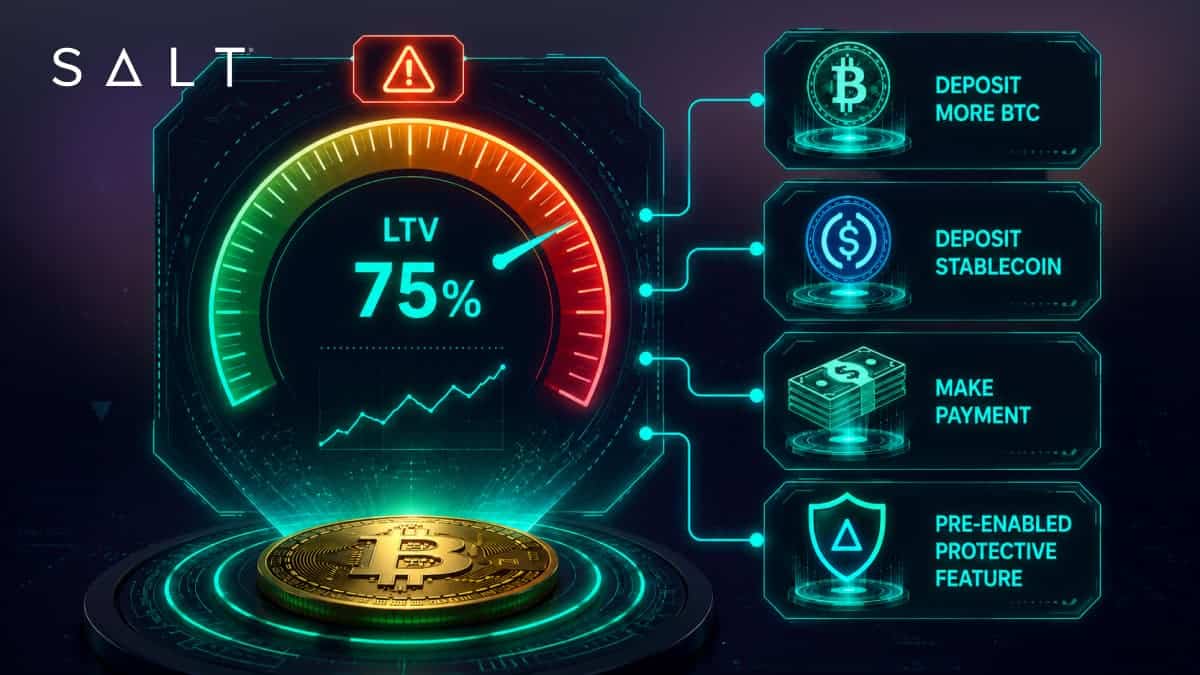

A margin call on a crypto-backed loan is a notice from your lender that the value of your crypto collateral has fallen far enough, relative to what you owe, that you need to restore the loan to a safer level. You can usually respond by adding more collateral, paying down part of the balance, or, on some platforms, relying on a built-in protective feature. If no action is taken and prices keep falling, the lender may sell some of your collateral to bring the loan back in line.

Below, we break down how margin calls work, the central role of loan-to-value (LTV), the difference between a margin call and a liquidation, and the practical steps you can take to avoid one in 2026.

What Is a Margin Call on a Crypto-Backed Loan?

When you take a crypto-backed loan, you put up crypto such as Bitcoin as collateral and receive cash or a stablecoin in return. Because crypto prices move constantly, the value of that collateral changes day to day. Lenders track the relationship between what you owe and what your collateral is worth using a metric called loan-to-value, or LTV.

When collateral value drops enough that your LTV climbs past a set threshold, the lender issues a margin call: a request to bring your loan back to a healthier ratio. Think of it as an early warning system rather than an automatic loss of your assets. It gives you the opportunity to act before anything is sold.

How Loan-to-Value (LTV) Works

LTV is your loan amount divided by the current value of your collateral, expressed as a percentage. If you borrow $25,000 against $50,000 of Bitcoin, your LTV is 50 percent. As the price of your collateral falls, your loan balance stays the same, so your LTV rises. The higher the LTV climbs, the closer you move toward a margin call.

Here is how a $25,000 loan behaves as Bitcoin collateral loses value:

| Bitcoin collateral value | Loan balance | LTV |

|---|---|---|

| $50,000 | $25,000 | 50% |

| $42,000 | $25,000 | about 60% |

| $35,000 | $25,000 | about 71% |

| $28,000 | $25,000 | about 89% |

Figures are illustrative only. The key takeaway: a lower starting LTV gives you more cushion before a margin call becomes a concern.

What Triggers a Margin Call?

The most common trigger is a decline in the market price of your collateral, which pushes your LTV upward. Adding to your outstanding balance can also raise LTV, and on some products accrued interest plays a role as well. Each lender sets its own maintenance threshold, so the exact LTV that triggers a margin call varies from platform to platform. The underlying mechanic is always the same: a margin call happens when your LTV crosses the line the lender has defined as too high.

What Happens During a Margin Call, Step by Step

- Notification. You receive an alert, typically by email and inside your loan dashboard, letting you know your LTV has crossed the threshold.

- A window to act. You are given an opportunity to bring your loan back to a healthier ratio.

- Your options. Deposit more collateral, make a payment to reduce your balance, or let a protective feature step in — if you enabled one ahead of time.

- If no action is taken. If prices keep falling and the loan is not restored, the lender may sell part of your collateral to bring the LTV back in line.

Margin Call vs. Liquidation: What Is the Difference?

These two terms are often used interchangeably, but they are not the same thing. A margin call is the warning and the request to act. Liquidation is the actual sale of collateral that can happen if the loan is not restored. In other words, a margin call is your chance to act, and liquidation is the consequence of not acting or of a very fast, severe market drop.

| Margin call | Liquidation |

|---|---|

| A notice that your LTV has climbed too high | The actual sale of collateral to repay part or all of the loan |

| You still hold your collateral | Some or all of your collateral is sold |

| You can restore the loan by adding collateral or paying down the balance | The lender takes the action to bring the loan back in line |

| A chance to act | The consequence of not acting, or of a very fast, severe drop |

The practical difference matters: respond to a margin call in time and you keep your position intact.

How to Avoid a Margin Call

- Start with a lower LTV. Borrowing at a conservative ratio builds in a larger price cushion before a margin call becomes a risk.

- Monitor the market and your dashboard. Keep an eye on your LTV so a downturn never catches you off guard.

- Set alerts. Price and LTV notifications give you time to react early.

- Keep extra collateral ready. Having assets on hand to deposit quickly can stop a margin call from escalating.

- Pay down during rallies. Reducing your balance when prices are strong lowers your LTV and your risk.

- Choose protective features. Some lenders offer tools designed specifically to reduce or remove liquidation risk.

How SALT Helps You Manage Margin Call Risk

Not all crypto lenders set their liquidation thresholds in the same place. Many platforms begin liquidating collateral once a loan reaches roughly the 60 percent to 80 percent LTV range, which means a normal market dip can force a sale. SALT sets its threshold at 90.91 percent LTV, well above much of the market, giving you considerably more room before your position is at risk.

You can borrow at LTV tiers of 30 percent, 50 percent, or up to 70 percent, and instead of selling the moment the market moves against you, two SALT features work to keep short-term volatility from forcing a sale of your collateral.

Stabilization. Powered by SALT’s proprietary STAMP™ execution engine, Stabilization automatically converts your crypto collateral to a US dollar stablecoin such as USDC when your LTV reaches that threshold, locking in its value during a downturn. Once you bring your LTV back to 83.33 percent or below through a payment or a collateral deposit, you are free to convert back into your chosen crypto mix and re-enter the market when the timing is right. SALT is the only lender offering portfolio stabilization of this kind.

SALT Shield®. This is a no-liquidation loan upgrade. For a one-time fee, SALT will forbear the triggering of margin calls and liquidation events for the remainder of your loan term, regardless of market swings, and your collateral stays in your account. Eligibility includes loans above $50,000, a current LTV under 70 percent, and enrollment at least three months before your loan matures. Availability also depends on your jurisdiction.

More room comes with responsibility: a higher threshold lets you borrow closer to the edge, so keeping a cushion still matters.

You can review current terms on the Rates & Fees page, and learn more about Stabilization and SALT Shield®. Product availability and eligibility vary by location, so check where SALT currently lends on the jurisdiction map before you plan around a specific feature.

EXPLORE SALT SHIELD® AND BORROW WITH CONFIDENCE

The Bottom Line

A margin call is not a penalty. It is a signal that your loan needs attention, and it usually comes with time to respond. Understanding LTV, watching your position, and borrowing at a conservative ratio go a long way toward keeping your collateral safe. And with features like Stabilization and SALT Shield®, you can take much of the market-watching stress out of the equation entirely.

Frequently Asked Questions

What LTV triggers a margin call on a crypto-backed loan?

There is no single industry-wide number. Each lender sets its own maintenance threshold, and the LTV that triggers a margin call depends on your loan terms and collateral type. The general rule holds across platforms: the higher your LTV climbs, the closer you are to a margin call, which is why a lower starting LTV is safer.

Do I lose my Bitcoin in a margin call?

Not automatically. A margin call is a notice, not a sale. You typically have the chance to add collateral or pay down your balance to restore your loan. Collateral is only sold if the loan is not brought back in line and prices continue to fall.

How much time do I have to respond to a margin call?

It depends on the lender and how quickly the market is moving. In a slow decline you may have a comfortable window, while a sudden, sharp drop can compress that time. Setting alerts and keeping extra collateral ready helps you respond quickly no matter the pace.

Is a margin call the same as liquidation?

No. A margin call is the warning that your LTV is too high. Liquidation is the actual sale of collateral that can follow if the loan is not restored. The margin call is your opportunity to act before liquidation becomes necessary.

At what LTV does SALT liquidate?

SALT is designed to give you more room than many lenders. Rather than selling your collateral as soon as the market dips, the Stabilization feature converts it to a US dollar stablecoin at 90.91 percent LTV to preserve its value, and you can re-enter the market once you bring your LTV back to 83.33 percent or below. With SALT Shield®, eligible loans are protected from forced liquidation for the remainder of the term. Exact terms depend on your loan and your jurisdiction.

Can I avoid margin calls entirely?

You can significantly reduce the risk by borrowing at a lower LTV, monitoring your loan, and keeping collateral in reserve. SALT also offers protective features: Stabilization can convert collateral to a stablecoin to preserve value during a downturn, and SALT Shield® can forbear margin calls and liquidations for the life of an eligible loan for a one-time fee.

What happens to my crypto when I repay the loan?

Once your loan is fully repaid, your collateral is released back to you. Borrowing against your crypto lets you access liquidity without selling, so you keep your holdings and your long-term position intact.

Disclaimer

This article is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Examples and figures are illustrative only. Borrowing against crypto collateral involves risk and may not be appropriate for your needs. Rates, features, and product availability are subject to change and may vary based on loan amount, LTV, collateral type, and your jurisdiction. SALT loans are subject to jurisdictional limitations and are not available everywhere. To see where SALT currently lends, visit saltlending.com/map-list. Digital currency is not legal tender, is not backed by the United States or any other government, and SALT accounts are not subject to FDIC or SIPC protections. SALT loans are originated by SALT Lending LLC (f/k/a SALT Master Fund II, LLC), NMLS 1711910. Please review your loan agreement and the Terms of Use for complete details.