Refinancing and transferring a crypto-backed loan means replacing your existing loan—often with a new lender—to get better terms, a lower rate, more breathing room before a margin call, or stronger protections for your collateral. Done right, you keep your Bitcoin invested while improving the terms you borrow against it.

If you’ve felt squeezed by your current lender—tight liquidation thresholds, rigid loan structures, or support that goes quiet when the market moves—you’re not stuck. This guide explains how to transfer a crypto loan , the signs to know when it’s worth switching, and what to evaluate before you move your collateral.

What Does It Mean to Transfer & Refinance a Crypto-Backed Loan?

Refinancing a crypto-backed loan is the process of paying off your current loan and opening a new one on better terms. The new loan can come from your existing lender or, more commonly, a different one that offers a lower rate, a more flexible structure, or better downside protection.

The mechanics are similar to refinancing a traditional loan. You keep ownership of your crypto throughout: rather than being sold, it simply moves from your old lender’s custody to your new lender’s. Because these loans are secured by your assets rather than your credit score, refinancing generally doesn’t require a credit check.

When Is It Worth Switching Crypto Lenders?

Switching is worth considering when your current loan is no longer serving your financial needs and goals or is costing you more money. The most common reasons borrowers refinance and transfer their crypto loan:

- Your rate is too high. If a competing lender will meaningfully beat your APR, the savings over your remaining term can be substantial.

- Your liquidation threshold is too tight. Lenders that trigger a margin call or forced sale at a low threshold leave little room for normal market volatility. A larger buffer means a routine dip is less likely to become a forced liquidation.

- Your loan structure is rigid. Fixed LTV options, inflexible repayment schedules, and one-size-fits-all terms may not fit your risk tolerance or goals.

- Your collateral is locked. Some platforms freeze your collateral until full payoff, so you can’t use it to make payments or lower your LTV when you need to.

- Support is hard to reach. When volatility hits, a ticket queue or a chatbot isn’t the same as a person who knows your loan.

- You have concerns about how your collateral is handled. How a lender custodies your assets—and whether it reuses them—directly affects your risk.

If one or more of these reasons describe your situation, refinancing and transferring your loan to a new lender may improve both your cost and your peace of mind.

How to Refinance & Transfer a Crypto Loan: Step by Step

The process is more straightforward than most borrowers expect:

- Review your current loan. Know your rate, balance, remaining term, LTV, and any prepayment or exit terms in your existing agreement.

- Compare lenders. Look beyond the headline rate at margin thresholds, custody practices, flexibility, fees, and support (see the next section).

- Get a quote on the new loan. A reputable lender will show you what your loan would look like—rate, terms, and LTV—before you commit.

- Open the new loan and move collateral. Once approved, your collateral secures the new loan and funds are issued, often within a day or two.

- Pay off the old loan. The new funds (or your freed-up liquidity) clear the prior balance, and your old collateral is released.

A good lender will walk you through this process rather than leave you to navigate the exit on your own.

What If All Your Collateral Is Tied Up in Your Current Loan?

One of the most common reasons borrowers feel stuck is that all of their Bitcoin is already committed to their existing loan—so there’s no spare collateral to open a new loan somewhere else. It can feel like your current lender is the only option simply because you’re fully invested.

This is exactly the kind of situation SALT is built to handle. With your authorization, our team can help bridge the payoff of your existing loan and free up your collateral, then open your new SALT loan against it—so a fully committed position doesn’t keep you locked in with a lender you’ve outgrown. Because every loan and platform is different, this is handled one-on-one: our team walks you through exactly what’s involved and manages the heavy lifting from there.

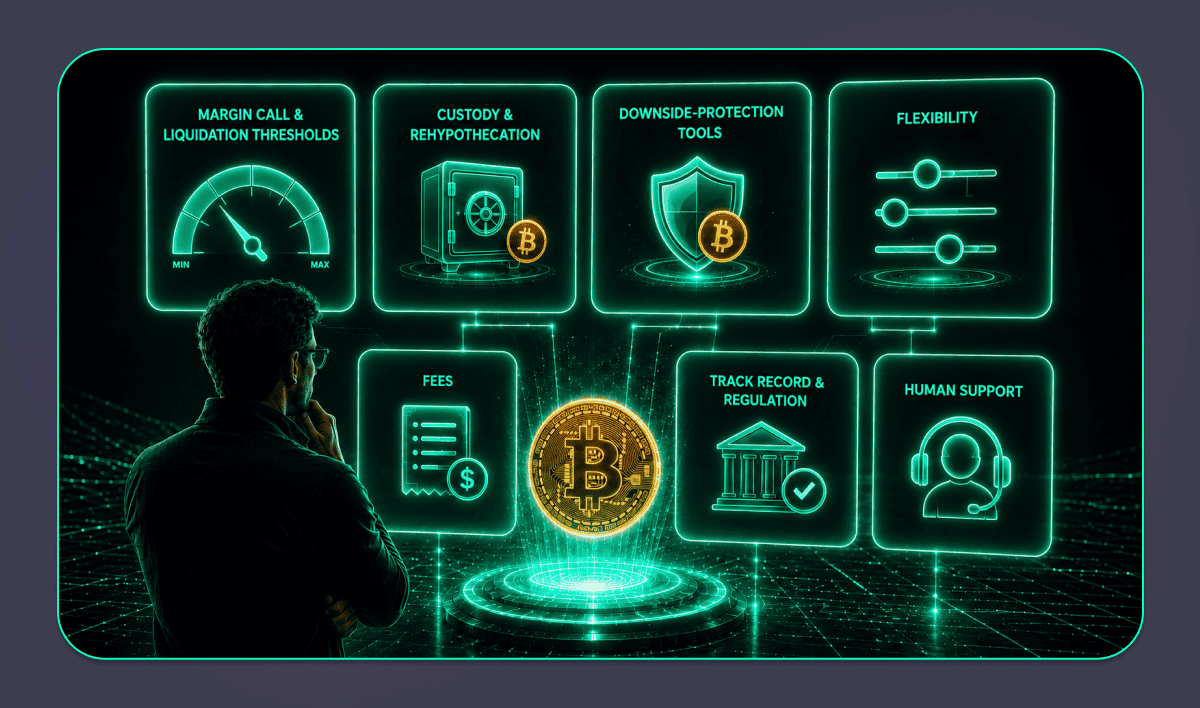

What to Look for in a New Lender

The cheapest rate isn’t always the best deal. Before refinancing, weigh these factors together:

- Margin call and liquidation thresholds. How far does the market have to move before you face a margin event? A larger buffer gives you more time to react.

- Custody and rehypothecation. Find out whether your collateral is held in qualified custody and whether the lender reuses (rehypothecates) it. A lender that does not lend out or trade your collateral carries different risk than one that does.

- Downside-protection tools. Some lenders offer features designed to help you manage volatility—structured rebalancing options or the ability to reduce or eliminate margin-call risk—rather than simply liquidating when a threshold is hit.

- Flexibility. Can the loan be structured around your LTV preference, term, and repayment style?

- Fees. Watch for origination, prepayment, withdrawal, and custody fees that erode the value of a lower rate.

- Track record and regulation. How long has the lender operated, through how many market cycles, and under what licenses and jurisdiction?

- Human support. When markets are volatile, access to a real expert matters more than a fast website.

Limited-Time Offer: Switch to SALT and We’ll Beat Your Rate by 1.5%

Currently borrowing with Ledn, Strike, Arch, or Unchained? SALT will beat your current rate by 1.5% when you refinance.* The consultation is free, with no obligation—tell us what you’re paying now and we’ll show you what switching would look like.

*Available for new borrowers switching from Ledn, Strike, Arch, or Unchained. Restrictions apply; promotion may be modified or discontinued at any time without notice. Schedule a consultation to confirm eligibility.

Why Borrowers Switch to SALT

SALT has originated Bitcoin-backed loans since 2016, making it one of the longest-running platforms in crypto lending—built and refined across multiple market cycles. Borrowers who refinance to SALT typically point to a few things:

- Room to breathe. SALT loans are designed so it takes a larger market move to trigger a margin event, giving you more time to respond.

- Your Bitcoin stays your Bitcoin. Collateral is held in qualified custody and is not rehypothecated, traded, or lent out while it backs your loan.

- Tools built for volatility. Stabilization offers structured options to rebalance your loan during sharp downturns without penalties, and SALT Shield™ lets qualifying borrowers reduce margin-call risk for the remainder of their loan term. SALT Shield™ is available on qualifying loans over $50,000 with an LTV under 70%, and can be activated up to three months before maturity.

- Transparent, low fees. No origination, prepayment, or custody fees, with APRs starting from 0.95%.*

- Real people. Dedicated support from a team that knows crypto lending—not a ticket number.

- US-regulated. SALT operates under US jurisdiction with the licenses required to lend and service loans where it’s approved. (NMLS #1711910)

Is Refinancing Right for You?

Refinancing makes the most sense when the new terms clearly outweigh the cost and effort of switching—lower rate, more collateral protection, better fit, or all three. Run the numbers on your remaining term, factor in any exit terms on your current loan, and consider how each lender handles your collateral and the moments when the market moves against you.

The best way to know is to compare your current loan side by side with an alternative. A reputable lender will give you that picture for free, with no obligation, so you can decide on your own terms.

Frequently Asked Questions

Does refinancing a crypto loan require a credit check?

Typically no. Crypto-backed loans are secured by your collateral rather than your credit history, so SALT does not require a credit check to refinance.

Will refinancing make me sell my Bitcoin?

No. The point of refinancing a crypto-backed loan is to keep your Bitcoin invested while improving your terms. Your collateral secures the new loan and is returned when that loan is repaid.

How long does it take to switch crypto lenders?

It varies by lender and your current loan, but once approved, SALT loans are often funded within 24–48 hours. The main variable is usually the exit terms on your existing loan.

Is it hard to leave my current lender?

Some lenders add friction when you decide to leave. SALT’s team has helped borrowers navigate exits from other platforms and will walk you through reviewing your current contract and mapping the switch step by step.

What happens to my Bitcoin while it’s collateral at SALT?

Your Bitcoin is held in qualified custody with institutional-grade security. It is not rehypothecated, traded, or lent out while it backs your loan.

How do I know if SALT is available where I live?

Availability varies by jurisdiction. Check current state and country coverage on SALT’s jurisdiction map at https://saltlending.com/map-list.

*Available rates and terms are subject to change and may vary based on loan amount, qualifications, jurisdiction, and collateral profile. Other terms, conditions, and restrictions may apply. Products, services, and promotions are not available in all jurisdictions; for current availability, see https://saltlending.com/map-list. Borrowing against collateral entails risk and may not be appropriate for your needs and is subject to margin calls and potential loss of collateral in volatile markets. Digital currency is not legal tender, is not backed by any government, and SALT accounts are not subject to FDIC or SIPC protections. This article is for educational and informational purposes only and does not constitute financial, investment, tax, or legal advice; you are encouraged to consult your own advisors before making financial decisions. SALT loans are originated by SALT Lending LLC — NMLS #1711910.