If you are considering borrowing against your Bitcoin, the single most important question is not the interest rate or the loan-to-value ratio. It is this: what happens to my Bitcoin while the loan is open? The crypto lending failures of 2022 taught borrowers a hard lesson. Platforms that reused customer collateral for their own trading and lending activities collapsed, and many customers lost assets they believed were secure.

No loan is without risk, but borrowers can evaluate how any lender handles collateral by asking a handful of specific questions. This guide explains how collateral custody works in a Bitcoin-backed loan, what rehypothecation means and why it matters, how regulation fits in, and the exact checklist to run before you sign a loan agreement.

Why Collateral Custody Is the First Question in Crypto Lending

A Bitcoin-backed loan is a secured loan. You transfer BTC or another supported digital asset to a lender as collateral, and the lender advances cash or stablecoins against it. When you repay the loan, your collateral is returned. The structure itself is centuries old. Securities-based lending in traditional finance works the same way.

What makes crypto lending different is custody. Your collateral leaves your wallet and sits with the lender or its custodian for the life of the loan. That means the lender’s practices, controls, and financial health directly affect whether you get your Bitcoin back. In 2022, several high-profile lending platforms froze withdrawals and entered bankruptcy after using customer assets to fund risky yield strategies. Borrowers with outstanding loans became unsecured creditors in lengthy court proceedings.

Those failures were not caused by Bitcoin. They were caused by business models that treated customer collateral as working capital. Understanding that distinction is the key to evaluating any lender today.

What Happens to Your Bitcoin When You Use It as Collateral

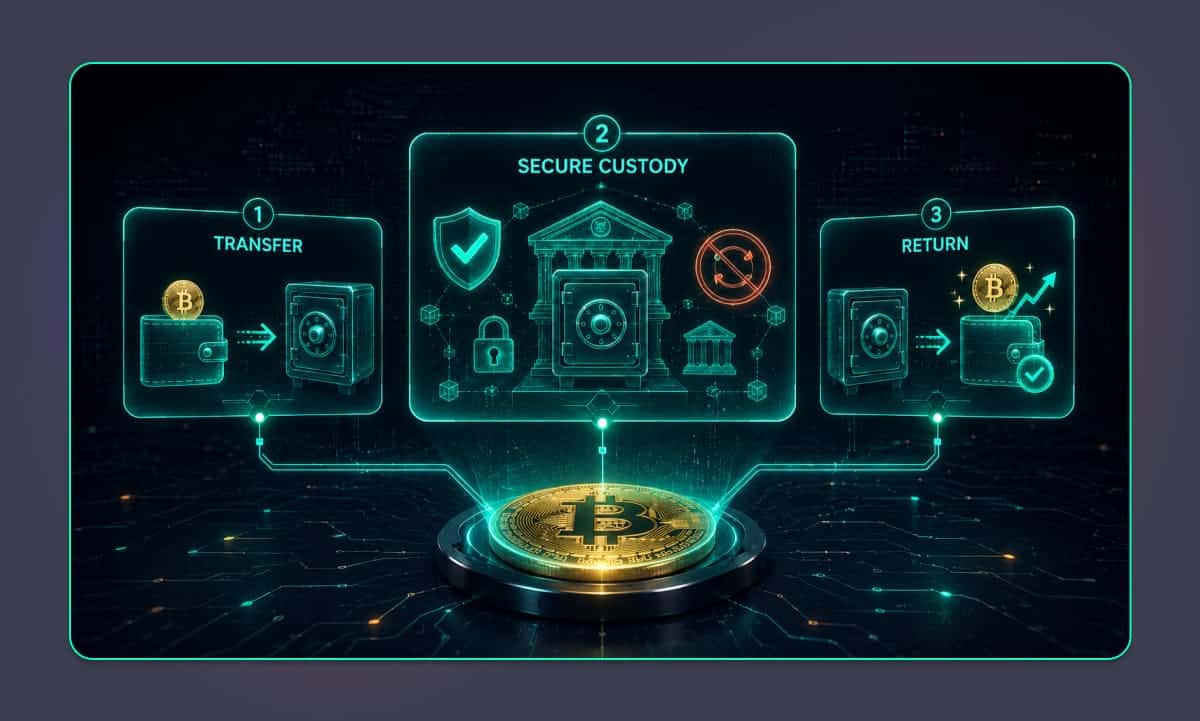

When you take out a Bitcoin-backed loan, your collateral typically moves through three stages:

- Transfer: You send your BTC to the lender’s custody environment. Ownership of the loan proceeds passes to you, and the collateral secures your obligation.

- Holding: The collateral is held in custody for the duration of the loan. This is the stage where lender practices diverge sharply. Conservative lenders hold collateral in institutional-grade custody and use it only in connection with the borrower’s loan. Others have historically lent out or traded customer collateral to generate additional revenue.

- Return: When you repay principal and any accrued interest, the collateral is released back to your wallet. If the market moved in your favor during the loan, you keep all of that appreciation because you never sold.

The holding stage is where you should focus your due diligence. The question to ask any lender is simple: is my collateral used for anything other than securing my loan?

Rehypothecation: The Word Every Borrower Should Know

Rehypothecation is the practice of a lender reusing customer collateral for its own purposes, such as lending it to third parties, posting it as collateral for the lender’s own borrowing, or deploying it in trading strategies. It is common in parts of traditional finance, where it is regulated and capped. In crypto lending, unrestricted rehypothecation was a central cause of the 2022 platform failures.

The risk is straightforward. If your lender reuses your collateral and its counterparties fail, your Bitcoin may not be there when it is time to return it. You are exposed not just to your lender, but to a chain of counterparties you never chose and cannot see.

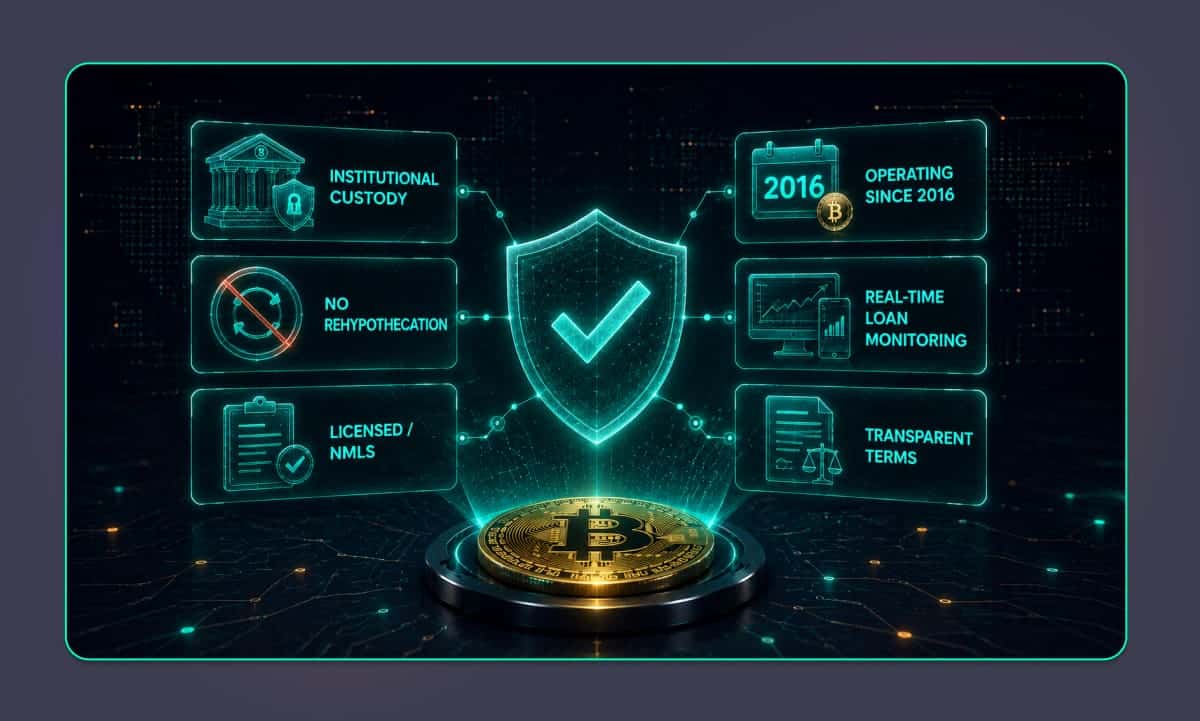

This is why a no-rehypothecation policy has become the dividing line between conservative and aggressive lenders. SALT does not rehypothecate borrower collateral. Collateral is held in institutional-grade custody, kept separate from SALT’s own treasury and operating funds, and is never re-lent, traded, or reused. It is used only to manage the borrower’s loan, a policy stated directly on the SALT personal loans page. When comparing lenders, ask for this commitment in writing and check whether it appears in the loan agreement itself, not just in marketing materials.

Regulation and Licensing: Why It Matters

Crypto lending sits within a patchwork of state and national regulation, and a lender’s licensing posture tells you a lot about its operating standards. Licensed lenders are subject to examinations, disclosure requirements, and consumer protection rules that unlicensed offshore platforms simply are not.

SALT has been operating since 2016, making it one of the longest-running lenders in the industry. SALT loans are originated by SALT Lending LLC, NMLS 1711910, and the company maintains state lending licenses that you can review on the SALT licenses page. Longevity matters here. A lender that operated through multiple full market cycles, including the 2022 credit crisis that took down many of its competitors, has demonstrated that its risk model works under stress.

Counterparty Risk vs. Market Risk: Two Different Questions

The risks in crypto lending fall into two categories, and borrowers should evaluate them separately.

Counterparty risk is the risk that the lender fails or mishandles your collateral. You can reduce it, though never eliminate it, by evaluating a lender’s licensing, collateral policies, custody practices, and operating history before you borrow.

Market risk is the risk that Bitcoin’s price falls while your loan is open. Because the loan is secured by volatile collateral, a sharp drop can push your loan-to-value ratio above contractual thresholds, triggering a margin call or, in severe cases, liquidation of collateral to protect the loan. This risk exists with every crypto lender. What differs is the tooling you get to manage it.

SALT gives borrowers several tools designed to help manage market risk:

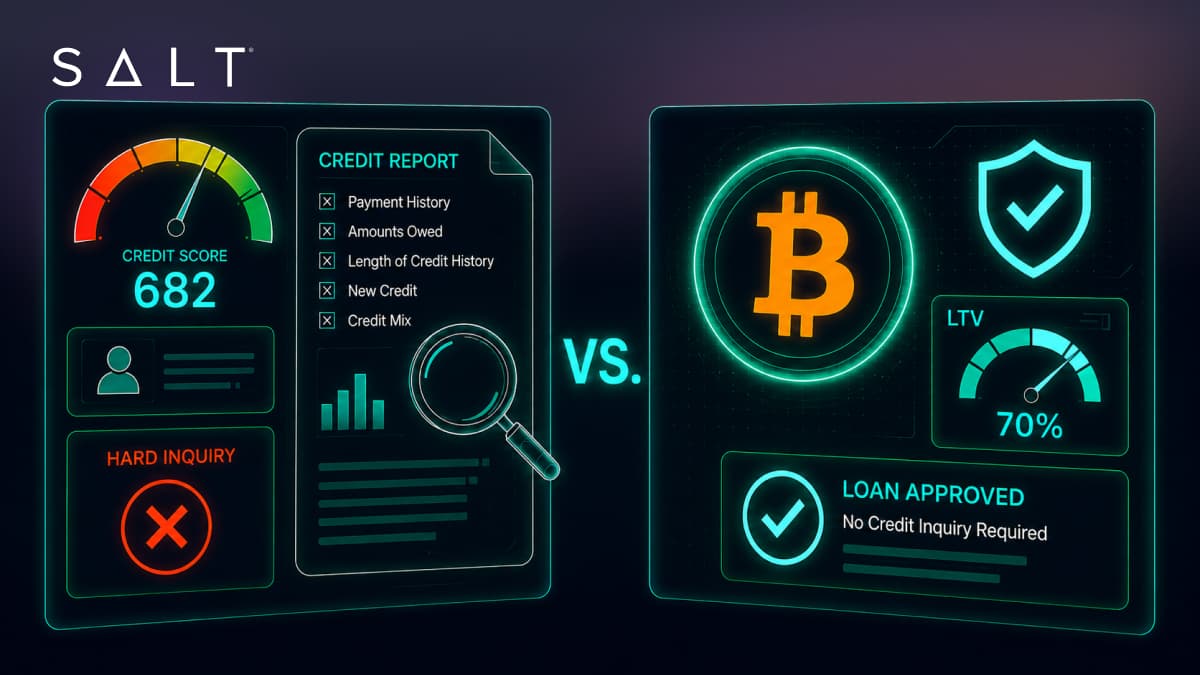

- Conservative starting LTVs: Loans are available at 30%, 50%, or 70% LTV. Borrowing at a lower LTV builds in a larger price cushion before any margin event.

- Real-time monitoring: The SALT app includes an LTV monitor and real-time alerts, so a market move never catches you off guard.

- Stabilization: During severe downturns, SALT’s Stabilization feature converts collateral to USDC to preserve its value rather than selling it off, giving you the option to re-enter the market later.

- SALT Shield: Eligible loans can add SALT Shield, which is designed to protect against market-triggered liquidation.

A Borrower’s Checklist for Vetting Any Crypto Lender

Before signing with any lender, including SALT, run through these questions:

- Does the lender rehypothecate collateral? Look for a clear no, stated in the loan agreement.

- How is collateral held? Look for institutional-grade custody that is kept separate from the lender’s own funds and never re-lent or traded.

- Is the lender licensed? Check for an NMLS number and state licenses you can verify independently.

- How long has the lender operated? Surviving the 2022 credit crisis is a meaningful signal.

- What happens in a downturn? Ask about margin call thresholds, cure periods, notification methods, and whether tools exist to avoid forced liquidation.

- Are the terms transparent? Rates, fees, LTV thresholds, and repayment options should be published, not revealed after you apply.

- Can you monitor your loan in real time? You should never learn about a margin event after the fact.

- What are the withdrawal and repayment mechanics? Prepayment should be penalty-free, and collateral return timelines should be defined.

If a lender hesitates on any of these, especially the rehypothecation question, keep looking.

The Bottom Line

Every loan involves risk, and Bitcoin-backed loans are no exception. The losses that hurt borrowers in the past, however, came primarily from lenders that reused customer collateral, not from the loan structure itself. The structure lets you access liquidity without selling, without a credit check, and without triggering a taxable sale in many jurisdictions. Understanding a lender’s licensing, collateral policies, and custody practices, borrowing at a conservative LTV, and monitoring your loan actively all help reduce, though never eliminate, the risks involved. If you want to see how the numbers look for your holdings, try the Bitcoin loan calculator or create a free SALT account to view live rates in about a minute.

Frequently Asked Questions

Are Bitcoin-backed loans safe?

No loan is risk-free, and Bitcoin-backed loans carry both counterparty risk and market risk. The largest borrower losses in 2022 came from platforms that reused customer collateral for their own trading and lending. Key factors to evaluate before borrowing include whether the lender is licensed, whether it rehypothecates collateral, how collateral is held, and what tools exist to manage market volatility. A lender that holds collateral in institutional-grade custody, separate from its own funds, and never re-lends it reduces that specific risk.

What is rehypothecation in crypto lending?

Rehypothecation is when a lender reuses your collateral for its own purposes, such as lending it out or posting it against the lender’s own obligations. It exposes you to counterparties you never chose. SALT does not rehypothecate borrower collateral; it is used only to manage the borrower’s own loan.

What happens to my Bitcoin when I use it as collateral?

Your Bitcoin is transferred to the lender’s custody and held there for the life of the loan. At SALT, collateral is held in institutional-grade custody, kept separate from company funds, and never re-lent. When you repay the loan, the collateral is returned to you, including any price appreciation that occurred while the loan was open, because you never sold your position.

Can I lose my Bitcoin with a crypto-backed loan?

There are two ways collateral can be lost: lender failure and market liquidation. Lender risk can be reduced by evaluating licensing, custody practices, and rehypothecation policies. Market risk can be reduced by borrowing at a lower LTV and responding promptly to margin alerts. SALT also offers Stabilization, which converts collateral to USDC during severe downturns to help preserve its value, and SALT Shield for eligible loans. Neither risk can be eliminated entirely.

Is SALT Lending regulated?

SALT loans are originated by SALT Lending LLC, NMLS 1711910, and SALT maintains state lending licenses, which are listed on its licenses page. SALT has operated continuously since 2016.

Does taking a Bitcoin-backed loan require a credit check?

No. Because the loan is fully secured by your digital assets, SALT does not check your credit. Approval is based on your collateral, and funding typically arrives within 24 to 48 business hours.

Disclaimer

This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Borrowing against collateral entails risk and may not be appropriate for your needs. Rates, terms, and product features are subject to change and may vary based on loan amount, qualifications, and collateral profile. SALT loans are subject to jurisdictional limitations and other restrictions, and loan terms may not be available in your jurisdiction. To see where SALT currently lends, visit saltlending.com/map-list. Digital currency is not legal tender, is not backed by the United States or any other government, and SALT accounts are not subject to FDIC or SIPC protections. SALT loans are originated by SALT Lending LLC (f/k/a SALT Master Fund II, LLC), NMLS 1711910. Consult your financial, tax, or legal advisors before making any borrowing decisions.