Key Takeaways

- When bitcoin prices fall, loan-to-value (LTV) increases automatically, raising risk.

- Loans move through stages — from stable, to margin call, to critical LTV at 90.91%.

- By default, loans without Stabilization enabled are subject to liquidation procedures defined in the loan agreement when LTV reaches critical levels.

- Stabilization is an opt-in feature borrowers can enable. When turned on, bitcoin collateral is converted to USDC in lieu of liquidation at 90.91% LTV (3% processing fee applies).

- Borrowers can add collateral or pay down principal to restore loan health.

- Interest accrual increases risk over time, even in flat markets.

- Loan structure determines resilience — lower starting LTV means greater flexibility.

- Eligible loans can add SALT Shield™, an optional upgrade that forbears margin call enforcement for the loan term.

When the Market Moves, Everything Becomes Clear

There is a moment that defines every bitcoin-backed loan.

It doesn’t happen when the loan is approved. It doesn’t even happen when the funds arrive.

It happens when bitcoin drops.

What felt like a well-structured financial decision suddenly demands attention. The numbers shift. Your loan-to-value ratio begins to climb. Notifications arrive. And the question becomes immediate:

What happens next?

For many borrowers, this is where uncertainty sets in. For experienced ones, it is where preparation takes over.

A decline in bitcoin’s price is not an edge case. It is part of the asset’s nature. The difference lies in how the loan has been structured and configured before that decline arrives. Most borrowers assume the risk in bitcoin-backed lending comes from the market.

In reality, it comes from how the loan is managed once the market moves—and which protective features the borrower has chosen to enable.

The Immediate Impact: Your Loan Changes Without You Doing Anything

When bitcoin’s price falls, your loan changes automatically. Not structurally, but mathematically.

Your collateral is worth less. Your loan balance remains the same. The relationship between the two—your loan-to-value ratio (LTV)—tightens.

This shift happens instantly. There is no delay, no buffer period, no negotiation. The system simply recalculates.

A loan that began at a comfortable level can move into a riskier position in a matter of hours during sharp market moves.

This is why bitcoin-backed lending feels different from traditional borrowing. It is not static. It responds in real time.

How SALT Handles Price Drops

SALT loans include several mechanisms that engage at different points on the LTV curve. Some are standard on every loan; others are optional features the borrower chooses to enable or add.

Loan Health Alerts and Margin Calls (Standard)

As pledged bitcoin declines in value, your LTV rises. SALT issues loan health alerts as LTV approaches predefined thresholds. If LTV reaches the Margin Call threshold, SALT issues a margin call requiring the borrower to either add collateral or reduce the loan balance to restore a healthier position.

What Happens at Critical LTV (90.91%) Depends on Your Configuration

If LTV continues to rise and reaches 90.91%, what happens next depends on whether the borrower has enabled Stabilization.

Important — Stabilization is Opt-In

Stabilization is an optional feature that the borrower must turn on in their SALT account. It is not enabled by default. Loans that do not have Stabilization turned on are subject to the liquidation procedures defined in the loan agreement when LTV reaches critical levels — which can include the sale of bitcoin collateral at then-current market prices. If you intend to use Stabilization, confirm it is enabled before market stress arrives.

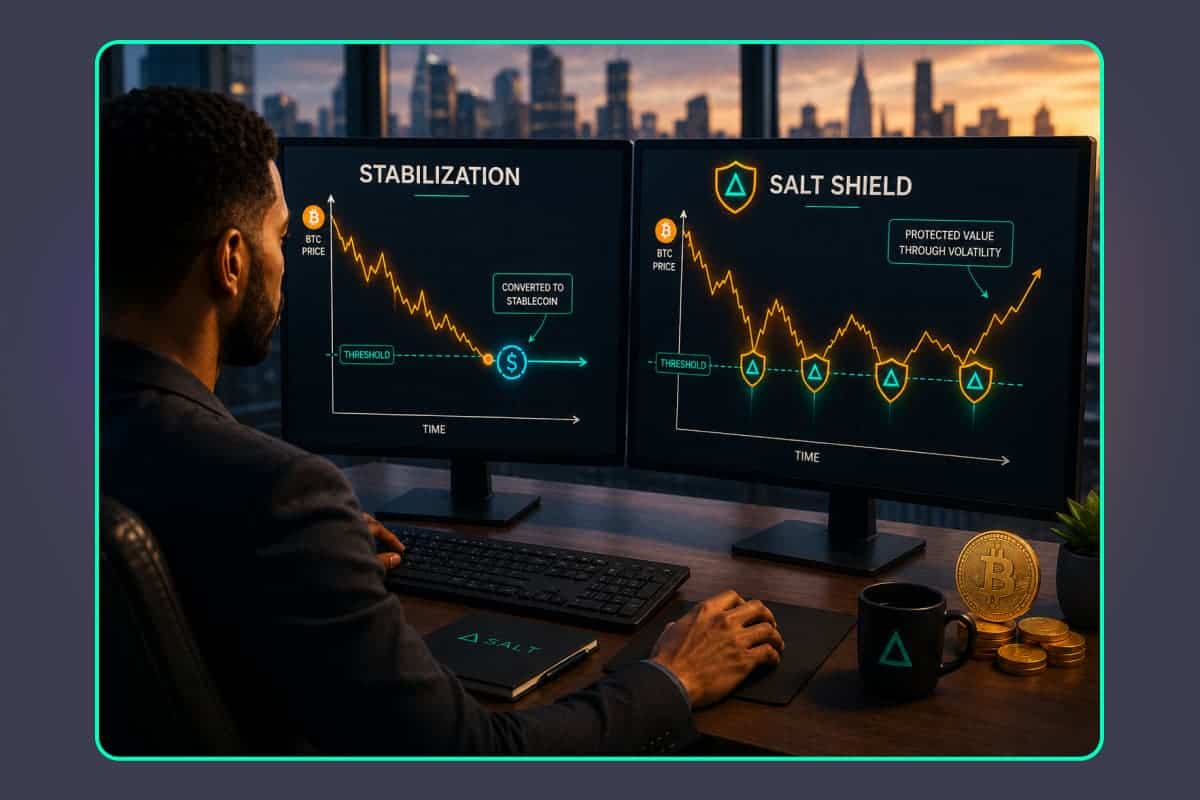

Stabilization (Opt-In)

Stabilization is an opt-in feature borrowers can enable from their SALT account. When Stabilization is turned on and LTV reaches 90.91%, SALT converts the borrower’s bitcoin collateral into a U.S. dollar stablecoin (USDC) in lieu of open-market liquidation. The conversion is designed to preserve the dollar value of the collateral at the moment of conversion rather than selling into a falling market. A 3% processing fee applies when Stabilization is triggered.

Without Stabilization Enabled

If Stabilization is not enabled and LTV reaches the critical threshold, the loan is subject to the liquidation procedures set out in the loan agreement. In practice, that can include the sale of bitcoin collateral at then-current market prices to restore the loan to compliant levels—meaning the borrower may realize losses that Stabilization would have helped them avoid.

SALT Shield™ (Optional No-Liquidation Upgrade)

SALT Shield™ is a separate optional loan upgrade. For a one-time fee on eligible loans, SALT forbears margin call and Stabilization enforcement for the loan term, subject to eligibility requirements, pricing, and the Shield Terms and Conditions. SALT Shield™ is a contractual forbearance—not an insurance product.

The Stages of a Decline: From Stability to Pressure

As bitcoin declines, a loan typically moves through recognizable phases. The progression is not abrupt—but it is also unforgiving if ignored. The outcome at the critical stage depends on whether Stabilization has been enabled.

| Stage | LTV Range | If Stabilization is OFF | If Stabilization is ON |

|---|---|---|---|

| Stable | Well below margin call threshold | Position absorbs normal market noise | Position absorbs normal market noise |

| Watch | Approaching threshold | Loan health alerts begin | Loan health alerts begin |

| Margin Call | At defined Margin Call LTV | Formal margin call issued; recommended that borrower adds collateral or pay down principal | Formal margin call issued; recommended that borrower adds collateral or pay down principal |

| Critical | 90.91% | Liquidation procedures under the loan agreement may apply, which can include the sale of collateral | Bitcoin collateral is converted to USDC in lieu of liquidation |

The earlier in this progression a borrower responds, the more optionality they preserve. The two right-hand columns make the point starkly: the same market move produces very different outcomes depending on a single account setting.

Volatility Is Expected. Unpreparedness Is Optional.

Periods of rapid growth are often followed by corrections. These corrections can be sharp, sometimes occurring over days rather than months. A decline of twenty to thirty percent is not unusual in this market.

For borrowers, this is not a flaw in the system. It is the system.

The real question is not whether bitcoin will fall at some point during the life of a loan. It is whether the loan has been structured, configured, and managed in a way that can withstand that fall.

Borrowers who enter a loan with a clear understanding of volatility tend to approach it differently. They leave room for movement. They anticipate scenarios. They build flexibility into their position—and they turn on the features designed to protect them before they need them.

Those who do not often find themselves reacting to the market rather than navigating it.

What You Can Do When Prices Fall

When bitcoin declines, the options available to a borrower remain relatively simple. What changes—and what ultimately determines the outcome—is how early those options are used.

Consider a borrower who takes out a bitcoin-backed loan at a 50% LTV. They pledge $100,000 in bitcoin and borrow $50,000. At the outset, the position is balanced, with a reasonable buffer against volatility.

If bitcoin falls by 20%, the collateral value drops to $80,000. The loan balance remains $50,000, but the LTV has now risen to 62.5%. At this stage, the loan is still manageable, but the margin for error has narrowed.

If the market declines further, by 30% from the original value, the collateral falls to $70,000. The LTV now rises to over 71%, moving the loan closer to the margin call threshold. This is typically the point where action becomes necessary, not optional.

Option 1: Add collateral

By depositing more bitcoin, the borrower increases the total collateral value and reduces the LTV. Adding $10,000 in bitcoin at this stage would bring the collateral to $80,000, lowering the LTV back down to 62.5% and restoring a more stable position.

Option 2: Reduce the loan balance

A partial repayment can also restore loan health. Repaying $10,000 of the loan brings the balance to $40,000 against $70,000 in collateral—an LTV of approximately 57%. This improves the immediate risk profile and reduces the amount of interest accruing over time.

Option 3: Make sure Stabilization is enabled before you need it

Stabilization is not an emergency button you reach for when LTV is already at 90%. It needs to be turned on in advance to engage at the critical threshold. Borrowers who plan to rely on Stabilization should confirm the feature is active on their loan well before any sign of market stress.

The starting LTV matters more than the response

A borrower who begins at a more conservative 30% LTV—borrowing $30,000 against $100,000 in bitcoin—has significantly more room to absorb volatility. Even after a 30% market decline, their LTV would rise to approximately 43%, still well within a comfortable range and far from critical thresholds.

The principle is simple: the lower the starting LTV, the greater the flexibility during downturns.

In practice, the most effective response to falling prices is not a single action but a combination of awareness, preparation, configuration, and timing. Borrowers who monitor their position, enable the right features in advance, and act early—before thresholds are reached—retain control over their loan. Those who wait for recovery often find that their options have narrowed significantly.

The Less Obvious Risk: Time and Interest

Market declines are visible. Interest accumulation is not.

Even if bitcoin’s price stabilizes after a drop, the loan continues to evolve. Interest accrues daily, increasing the total balance. Over time, this can push the loan into a higher-risk position without any further movement in the market.

This is why downturns can have a lasting effect.

A borrower who does not account for time may find that their position becomes progressively tighter, even in a flat market environment.

Managing a loan effectively requires attention not just to price, but to duration.

Psychological Pressure and Decision-Making

One of the most underestimated aspects of a falling market is not technical. It is behavioral.

When prices decline, decision-making becomes more difficult. There is a natural tendency to wait, to hope for a rebound, to delay action in anticipation of recovery.

This hesitation can be costly.

Collateralized loans reward clarity and responsiveness. They are less forgiving of indecision. The earlier a borrower acts—and the earlier they configure their loan with the protections they want—the more control they retain over the outcome.

In this sense, collateral management is as much about mindset and configuration as it is about mechanics.

How Loan Structure Determines Your Experience

Not all loans respond to market declines in the same way.

A loan taken at a higher LTV will feel the effects of a downturn much sooner than one structured more conservatively. A loan with Stabilization enabled responds differently than one without. And a borrower without access to additional liquidity may have fewer options when action is required.

This is why the structure of the loan at the outset—and the features enabled within it—plays such a significant role.

Borrowers who want to understand how different LTVs, terms, and repayment strategies affect outcomes can explore this in more detail in our companion post on how volatility thresholds work in bitcoin-backed lending.

Borrowers who prioritize flexibility—through lower LTV ratios, available reserves, clear repayment plans, and the right protective features enabled in advance—tend to navigate volatility with greater confidence. Those who optimize purely for maximum borrowing often experience the opposite.

Comparing Your Optional Protections

Both Stabilization and SALT Shield™ are responses to the same underlying reality: bitcoin is volatile, and traditional lending models are not built to accommodate that volatility gracefully. Both are optional. The difference lies in what each one does and when it engages.

- Stabilization is an opt-in account feature available to borrowers at no upfront cost. When enabled, it triggers at the 90.91% critical LTV threshold by converting bitcoin collateral to USDC in lieu of liquidation (3% processing fee applies).

- SALT Shield™ is a paid loan upgrade on eligible loans. It forbears margin call enforcement and Stabilization conversion for the loan term, so short-term price movements do not trigger forced conversion at all.

A loan with neither feature enabled is subject to standard liquidation procedures under the loan agreement if LTV reaches critical levels and is not restored by the borrower.

A Different Way to Think About Market Drops

It is easy to view falling prices as a problem to solve.

A more useful perspective is to see them as a condition to plan for—and to configure for, before they arrive.

Bitcoin-backed loans are not designed for static markets. They are designed for movement. The borrowers who succeed within this framework are not those who avoid volatility, but those who understand how to operate within it and have enabled the protections they want before they need them.

When bitcoin falls, the loan reveals its structure. It shows how much flexibility exists, how prepared the borrower is, and how effectively the position has been configured and managed.

The market does not change the loan. It exposes it.

The borrowers who understand this are the ones who remain in control when others are forced out.

Frequently Asked Questions About Bitcoin Price Drops

What happens if bitcoin drops during a loan?

When bitcoin’s price falls, the value of your collateral decreases while your loan balance remains the same. This causes your loan-to-value (LTV) ratio to increase, raising the risk level associated with your loan. If LTV reaches certain thresholds, the lender may issue a margin call or take protective action to rebalance the loan.

What is a margin call in a bitcoin-backed loan?

A margin call is a notification from your lender that your loan requires attention. It typically occurs when your LTV rises above a defined level due to a decline in bitcoin’s price. To restore balance, borrowers are usually required to either add more collateral or reduce their loan balance.

Is Stabilization automatic at SALT?

No. Stabilization is an opt-in feature that the borrower must enable in their SALT account. It is not active by default. Loans without Stabilization enabled are subject to the liquidation procedures defined in the loan agreement if LTV reaches critical levels. If you intend to use Stabilization, confirm it is turned on before market stress arrives.

What happens at 90.91% LTV at SALT?

If Stabilization is enabled, SALT converts the borrower’s bitcoin collateral into USDC at the 90.91% LTV threshold (3% processing fee applies), preserving dollar value at the moment of conversion. If Stabilization is not enabled, the loan is subject to the liquidation procedures defined in the loan agreement, which can include the sale of bitcoin collateral at then-current market prices.

How can I avoid liquidation when borrowing against bitcoin?

Start with a conservative LTV, actively manage your loan, and enable the protective features you want before market stress arrives. This includes monitoring your position, adding collateral when necessary, making partial repayments to lower your balance, and turning on Stabilization (or adding SALT Shield™ if eligible). Acting early—before thresholds are reached—gives you more control over the outcome.

Does interest increase my risk over time?

Yes. Interest accrues on your loan balance over time, gradually increasing the total amount owed. Even if bitcoin’s price remains stable, this can cause your LTV to rise, slowly increasing your risk level. Duration and repayment strategy are critical components of collateral management.

Is it safer to borrow at a lower LTV?

Generally, yes. A lower starting LTV provides a larger buffer against market volatility, allowing your loan to withstand price declines without reaching risk thresholds as quickly. Borrowers who prioritize lower LTVs tend to have more flexibility and more time to respond to market movements.

How does SALT help me manage volatility?

SALT provides flexible loan configurations, real-time monitoring, loan health alerts, the option to enable Stabilization (USDC conversion in lieu of liquidation at 90.91% LTV, 3% processing fee), and SALT Shield™ on eligible loans (forbears margin call enforcement for the loan term, for a one-time fee). Both Stabilization and SALT Shield™ are optional and require the borrower to opt in.

Are there tax consequences when Stabilization converts my bitcoin to USDC?

Conversions between bitcoin and USDC may be treated as taxable events in many jurisdictions. Tax treatment varies based on individual circumstance and applicable law. Borrowers should consult a qualified tax advisor.

Continue with your learning about bitcoin-backed lending by downloading our free playbook, The Borrower’s Guide: Bitcoin Volatility Protection Playbook.

Review Your Loan Options Today

Log in to your SALT account to review your available LTV tiers, confirm whether Stabilization is enabled on your loan, check SALT Shield™ eligibility, monitor your collateral health, and evaluate how your loan structure aligns with your volatility tolerance.

Related reading: How Volatility Thresholds Work in Bitcoin-Backed Lending • When Should You Borrow Against Bitcoin Instead of Selling?

Important Disclosures

This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Borrowing against bitcoin involves risk, including market volatility, margin call events, liquidation of collateral, and the potential loss of collateral. Past performance and historical market behavior are not indicative of future results.

Stabilization is an opt-in feature that the borrower must enable in their SALT account. Loans without Stabilization enabled remain subject to the liquidation procedures defined in the loan agreement, which may include the sale of collateral. Loan products, LTV options, interest rates, fees (including the 3% Stabilization processing fee), durations, and terms are subject to change and are governed by the loan agreement.

SALT Shield™ is subject to eligibility requirements, pricing, and jurisdictional restrictions that may change from time to time at SALT’s discretion; see the SALT Shield™ Terms and Conditions for complete details. SALT Shield™ is a contractual forbearance of SALT’s margin call rights for the Shield period—it is not an insurance product.

The conversion of bitcoin collateral to USDC under Stabilization, and any subsequent conversion back to bitcoin or other collateral, may have tax consequences depending on your jurisdiction. Consult a qualified tax advisor regarding your specific situation.

SALT products and services are not available in all jurisdictions. For the most current list of supported jurisdictions, please visit saltlending.com/map-list.