Disclaimer: This article is for informational purposes only and does not constitute financial, legal, or investment advice. Loan products are subject to eligibility, terms, and availability. Rates and thresholds are subject to change without notice.

You already know Bitcoin is worth holding. But did you know it can also unlock liquidity — without selling a single sat? This guide covers everything advanced borrowers need to know about LTV and margin calls in 2026.

Borrowing against Bitcoin isn’t new. But the landscape has changed dramatically. Markets have matured. Products are more sophisticated. Risk engines are better. And borrowers today are more strategic.

This advanced guide goes far beyond the basics of LTV and margin calls in Bitcoin-backed loans. If you’ve already read SALT’s original LTV explainer, you’re ready for the next level.

In this article, we’ll cover:

- How Loan-to-Value (LTV) really works

- How Bitcoin’s volatility impacts LTV

- Why crypto lenders use LTV instead of credit scores

- SALT’s current LTV options (30%, 50%, 70%)

- How Bitcoin’s market structure affects LTV changes

- What a margin call is and why it happens

- Liquidation thresholds and risk levels

- What happens during a margin call step-by-step

- Stabilization vs. liquidation

- How SALT Shield™ provides no-liquidation protection

- Advanced risk-management strategies

- Frequently asked questions (FAQs) on LTV and Margin Calls

1. What LTV Really Represents

What is LTV?

Loan-to-value (LTV) is a way of showing how much you’re borrowing compared to the value of the asset you’re using as collateral. It’s written as a percentage. In simple terms, LTV tells you the maximum amount you can borrow based on how much your asset is worth.

Here’s a simple example:

If your Bitcoin is worth $10,000 and the lender offers a 50% LTV, it means you can borrow up to 50% of the value of your Bitcoin.

So:

- Asset value: $10,000

- LTV: 50%

- Maximum amount you can borrow: $5,000

That’s how LTV works in practice.

Most describe Loan-to-Value (LTV) as a simple formula:

Loan Amount ÷ Collateral Value = LTV

That’s correct, but incomplete.

In practice, LTV is a dynamic risk indicator that moves:

- Every time Bitcoin’s price changes

- Every time you make a payment

- Every time you add or withdraw collateral

- Every time volatility spikes or liquidity thins

- Every time spreads widen across major exchanges

LTV is not a static metric — it is a moving risk barometer.

Why Bitcoin-Backed Lenders Use LTV Instead of Credit Scores

In traditional finance, lenders evaluate the borrower, not the asset. Every decision, from interest rates to loan approval, is driven by credit scores, income history, debt ratios, employment stability, and long-term financial behavior. In other words:

Legacy lending is built on judging you. Crypto-backed lending reverses that model entirely.

Crypto lenders evaluate the asset, not the person.

Instead of asking: “Can the borrower be trusted to repay based on their past behavior?”

The key question becomes: “Is the collateral strong enough to secure the loan today and over time?”

This shift makes collateralized crypto lending dramatically more inclusive and efficient:

- No credit checks

- No income documentation

- No years of financial history required

- Faster approvals

- Greater accessibility

- Fairer pricing based on transparent collateral ratios

For borrowers who are unbanked, self-employed, new to credit, or recovering from financial challenges, this model removes the biggest barrier to accessing liquidity.

This is where SALT has always been different

Since its founding in 2016, SALT has operated on a simple principle: your credit does not matter, your collateral does. That means a low credit score won’t disqualify you, missing traditional paperwork won’t slow you down, and your personal financial past doesn’t determine your ability to access liquidity today. You’re not penalized for being a first-time borrower, and your interest rate is based on your chosen LTV — not on subjective judgments about your credit history.

Instead of digging through your credit reports, SALT evaluates:

- The strength, value, and volatility of your crypto collateral

- Your chosen starting LTV

- The likely behavior of the asset during the life of the loan

- Your responsiveness during market volatility

- Your optional risk protections (Stabilization, SALT Shield™)

This creates a transparent, objective, borrower-first lending experience grounded in the mathematics of collateral rather than subjective credit scoring.

The outcome is a fairer, faster, and more predictable lending model

By focusing on collateral instead of credit scores, SALT enables borrowers to unlock liquidity without navigating traditional credit systems, while preserving their privacy and autonomy. It allows individuals with limited or no credit history to access funds and helps them avoid the punitive rates typically associated with “bad credit” loans. This approach provides a more reliable, transparent, and rules-based way to manage risk.

In short: crypto-backed loans aren’t about who you are — they’re about what you own and how responsibly you manage your collateral.

2. SALT’s Current LTV Options (2026 Update)

Based on SALT’s latest pricing and rate structure, borrowers can choose from three starting LTV tiers, each with different risk and liquidity characteristics.

30% LTV — Conservative

- Highest level of protection

- Lowest probability of margin calls

- Most resilient during BTC volatility

- Ideal for long-term borrowers and HODLers

- Available for 1, 3, or 5-year terms

- Interest rate: 8.95% (~9.95–12.95% APR — Subject to change without notice)

50% LTV — Standard / Balanced

- Greater liquidity while maintaining a reasonable buffer

- Appropriate for borrowers comfortable topping up collateral if needed

- Offers more leverage but still manageable during market swings

- Available for 1, 3, or 5-year terms

- Interest rate: 9.95% (~10.95–13.95% APR — Subject to change without notice)

70% LTV — Maximum Leverage

- Highest borrowing power

- Highest sensitivity to BTC price movements

- Best for active borrowers who monitor markets closely

- Carries increased margin call likelihood

- Available only for 1-year terms

- Interest rate: 13.45% (14.45% APR — Subject to change without notice)

3. Why Bitcoin’s Unique Market Structure Impacts LTV

Bitcoin isn’t like traditional collateral assets. Its price is affected by:

High Intraday Volatility — BTC can swing 5–10% within a single day.

Macro-driven volatility spikes — FOMC meetings, CPI announcements, ETF flow reports, mining difficulty adjustments, and more can cause dramatic price moves.

Liquidity cycles — During low-liquidity periods (holidays, weekends, global events), LTV can move faster.

Correlation shocks — BTC decouples from or sharply recouples with S&P 500 or Nasdaq indices.

Exchange fragmentation — BTC pricing varies across exchanges; lenders use oracle pricing. When one exchange spikes down temporarily, LTV may reflect consolidated price adjustments.

All of this means your LTV is alive. Understanding its motion is key to protecting your collateral.

4. How LTV Changes as Bitcoin’s Price Moves

When Bitcoin’s price increases, your collateral becomes more valuable, your LTV decreases, your loan becomes safer, and the likelihood of a margin call shrinks. Many long-term borrowers naturally see their LTV improve during sustained market growth. Conversely, when Bitcoin’s price falls, your collateral value decreases, your LTV rises, and you move closer to margin call thresholds. The speed and severity of this change often depend on how volatile the Bitcoin market is at the time.

For Example

- Loan amount: $35,000

- Starting LTV: 70%

- BTC price at deposit: $62,500

- Required BTC: 0.80 BTC (0.80 BTC × $62,500 = $50,000 collateral; $35,000 ÷ $50,000 = 70% LTV ✓)

If BTC price drops to $50,000:

- New collateral value: $40,000 (0.80 BTC × $50,000)

- New LTV: 87.5% (just below the liquidation threshold)

Even a modest price drop can push a 70% LTV loan dangerously close to forced liquidation. This is why conservative starting points — and close monitoring — matter.

5. What Is a Margin Call?

What is a crypto margin call?

A margin call is a notification that your LTV has exceeded its warning range and you must take action.

This can be triggered by:

- Price drops

- Market volatility

- Exchange spreads

- Flash crashes

- Oracle updates

Margin calls at SALT are structured, proactive, and designed to support borrowers. You’ll receive platform notifications, email alerts, and optional SMS or phone calls — all aimed at giving you enough time to take action and correct your LTV before liquidation becomes necessary.

6. Liquidation Thresholds Explained

The below outlines where margin events occur on SALT loans.

- Warning: ≥ 75% LTV

- Margin Call: ≥ 83.33% LTV

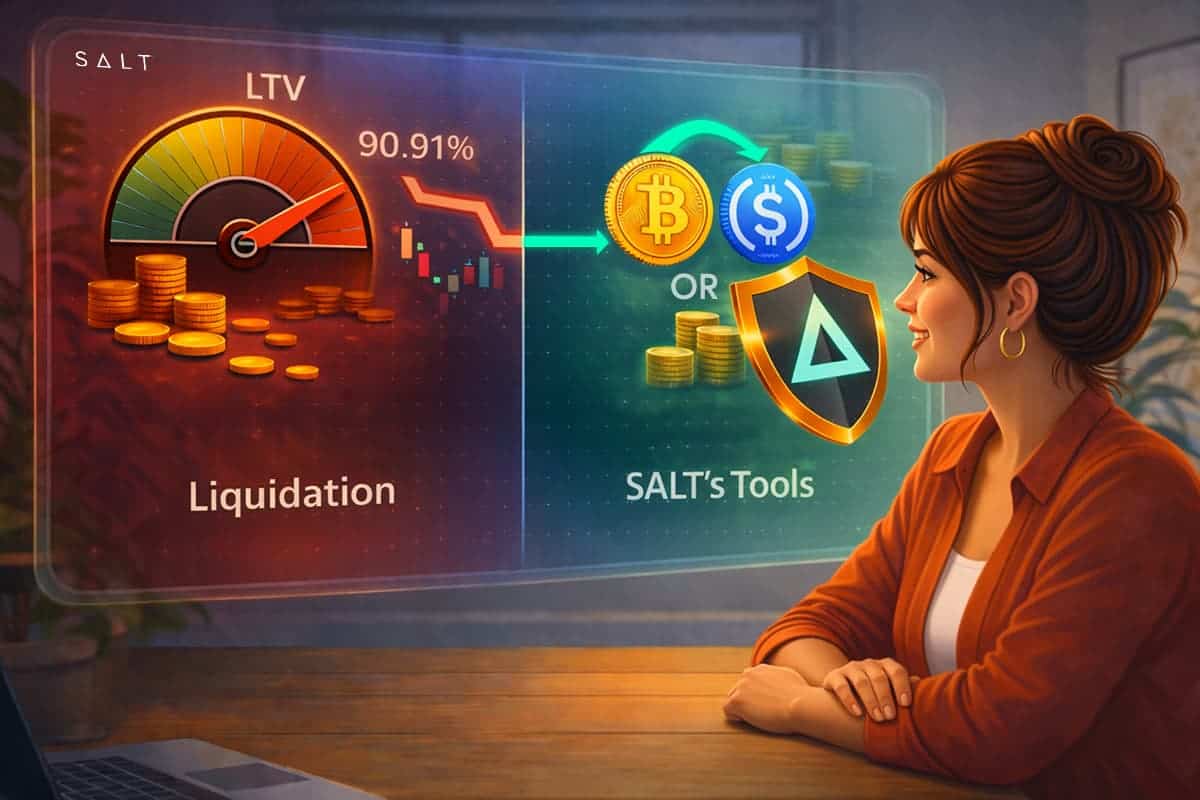

- Margin Event: ≥ 90.91% LTV

These are not the same as your starting LTV. The closer you are to 90.91% LTV, the closer you are to forced liquidation. This threshold exists to protect the borrower and lender in extreme market conditions.

7. What Actually Happens in a Margin Call (Step-by-Step)

When your LTV crosses a warning threshold:

Step 1: SALT notifies you Multiple channels → portal, email, phone.

Step 2: You choose one of several actions

- Add more Bitcoin or eligible collateral

- Pay down part of your loan

Step 3: LTV is recalculated immediately Your collateral buffer increases.

Step 4: If no action is taken When LTV reaches the liquidation boundary, SALT sells just enough collateral to restore safety.

SALT does offer volatility protection tools as outlined in the following two sections.

8. SALT Stabilization vs. Liquidation

Stabilization = Partial, strategic protection

Liquidation = Forced collateral sale to restore LTV safety

Stabilization helps:

- Prevent full liquidation

- Give you more time during volatility

- Reduce forced selling

Liquidation occurs when:

- LTV exceeds the liquidation threshold

- You take no protective action

- The market moves too quickly

SALT’s philosophy is: liquidation is the last resort, and we want to prevent it.

9. SALT Shield™: No Margin Calls. No Liquidation. No Stress.

If your loan qualifies — meaning the balance is over $50,000, the current LTV is below 70%, and the loan is more than three months from maturity — you can upgrade to SALT Shield™. Once activated, it removes all margin call notifications, and market-triggered liquidation risk for the rest of your loan term.In practice, SALT Shield™ converts your loan into a no-liquidation, volatility-protected product that keeps your Bitcoin collateral safe regardless of market conditions, for the entire remainder of your loan.

10. Advanced Risk-Planning Strategies Borrowers Use

Experienced borrowers follow disciplined rules:

Rule #1: Never use your entire BTC stack as collateral

Always maintain reserves for top-ups.

Rule #2: Keep starting LTV at conservative ranges (30–40%)

Higher LTV = more margin call probability.

Rule #3: Use multi-year loans to reduce short-term shocks

More time = more flexibility.

Rule #4: Monitor BTC macro events

- FOMC statements

- ETF flows

- Mining halvings

- Exchange outages

- CPI releases

Rule #5: Keep fiat liquidity accessible Useful for fast loan paydowns.

Rule #6: Consider SALT Shield™ for long-term holdings

11. Warning Signs Your LTV May Be at Risk

- BTC price drops 10–15% in a short window

- Exchange spreads widen

- Market liquidity thins

- Funding rates spike

- Macro markets panic (stocks, bonds)

- High-volatility news cycle

- Sudden BTC dominance weakness

Understanding these signals helps you respond before margin calls begin.

FAQs on LTV and Margin Calls

What is LTV in a Bitcoin-backed loan? Loan-to-value (LTV) measures risk by comparing the loan amount to the value of your Bitcoin collateral. Lower LTV produces fewer margin calls.

What LTV options does SALT offer? SALT currently offers three starting Loan-to-Value (LTV) options for Bitcoin-backed loans: 30%, 50%, and 70%. The 30% and 50% LTV tiers are available with 1-, 3-, or 5-year terms, while the 70% LTV tier is available on 1-year terms only and carries the highest sensitivity to market volatility.

What triggers a margin call? A margin call is triggered when your LTV rises past preset warning thresholds due to Bitcoin price volatility.

Can I prevent liquidation? Yes — by adding collateral, making loan payments, selecting Stabilization, or qualifying for SALT Shield™.

How are the LTV margin triggers determined? The Loan-to-Value margin requirements are determined by lenders and agreed to by borrowers. Terms are clearly outlined in each loan agreement. Thresholds may vary by loan program — always refer to your specific loan agreement for exact figures.

| Notification | LTV |

| First margin call warning | 75% |

| Second margin call | 83.33% |

| Final notice | 88% |

| Stabilization | 90.91% |

What happens if my LTV is over 70% at maturity? At maturity, your loan is due and payable regardless of the LTV. You may also refinance and enter a new loan with a new maturity date. In order to refinance your loan, however, you will need to meet standard LTV requirements at the time of refinancing. Once you enter into a new refinanced loan, you will then have the option to re-enroll your new loan in SALT Shield™, if you qualify.

Understanding LTV and Margin Calls

LTV isn’t just a number — consider it a living risk indicator. And margin calls aren’t failures; they’re alerts giving you time to protect your Bitcoin.

With SALT’s conservative LTV tiers, transparent warning thresholds, Stabilization option, and SALT Shield™ upgrade, borrowers can manage volatility confidently while retaining their long-term Bitcoin position.

Understanding LTV deeply lets you borrow strategically, stay protected, and maintain exposure to the long-term upside of Bitcoin — without needing to sell.

This article is for informational purposes only and does not constitute financial, legal, or investment advice. All loan products are subject to eligibility, credit approval, and applicable terms. Interest rates and LTV thresholds are subject to change without notice. SALT Lending products may not be available in all U.S. states or jurisdictions. Please review your loan agreement for complete terms and conditions.