Quick answer: Applying for a Bitcoin-backed loan from SALT does not involve a credit check, so there is no hard inquiry and no direct impact on your credit score when you apply. Your loan is secured by your crypto collateral, not your credit history. Because most crypto-backed loans are not reported to consumer credit bureaus, they generally do not appear on your credit report at all, which also means on-time payments typically will not build your credit.

One of the most common questions people ask before borrowing against Bitcoin is what it will do to their credit. It is a fair question. Nearly every other loan in your financial life, from a mortgage to a credit card, starts with a credit pull and ends up on your credit report. Bitcoin-backed loans work differently, and understanding why can help you decide whether this type of borrowing fits your situation. This guide explains what lenders like SALT actually evaluate, what happens (and does not happen) to your credit, and where the edge cases are.

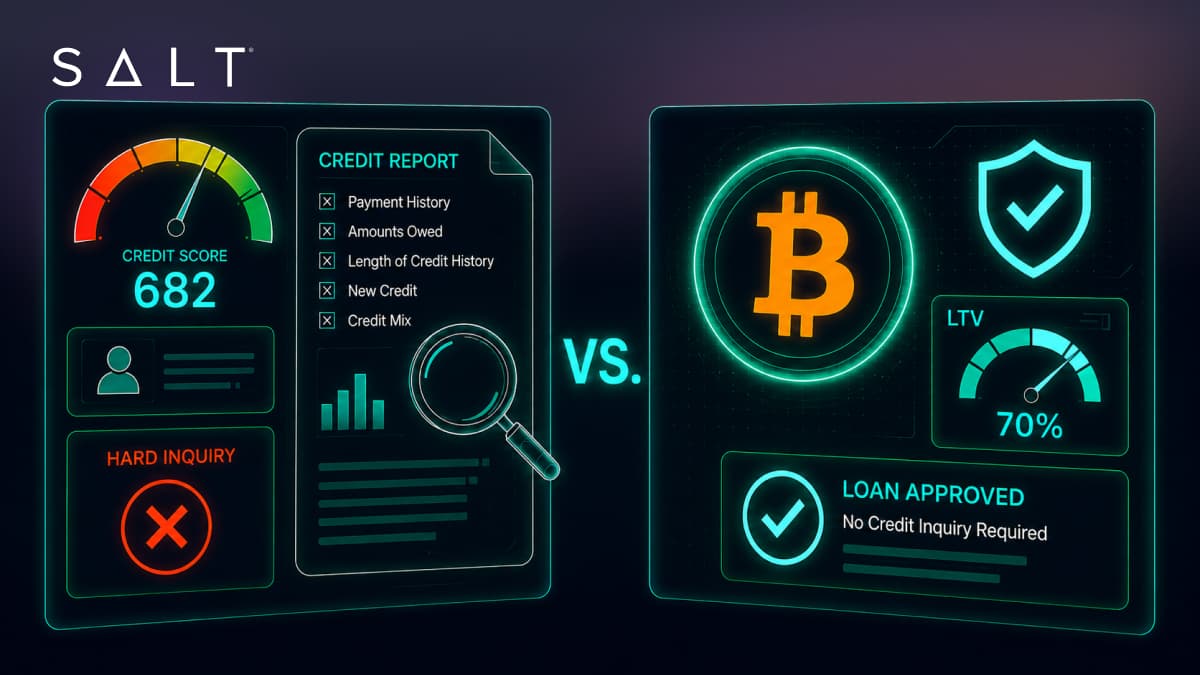

Why Bitcoin-Backed Lenders Do Not Check Your Credit

A credit score exists to answer one question for a lender: how likely is this person to repay an unsecured or under-secured debt? When a loan is fully secured by liquid collateral, that question matters far less. With a Bitcoin-backed loan, you pledge crypto worth more than the amount you borrow. If the loan is not repaid, the lender can look to the collateral rather than to a collections process.

That is why SALT’s underwriting is collateral based. There is no credit check at any point in the application. As we like to say, your crypto is your credit. Instead of pulling a credit file, SALT evaluates the value and type of the digital assets you pledge, and you choose a loan-to-value (LTV) ratio, currently up to 70%, that determines how much you can borrow against them. You can model this with the loan calculator.

This is also why Bitcoin-backed loans are accessible to borrowers a traditional lender might decline: self-employed people with irregular income, recent immigrants with thin credit files, or long-term holders whose net worth lives on-chain rather than in a FICO score.

Does Applying Trigger a Hard or Soft Inquiry?

Neither. A hard inquiry happens when a lender pulls your credit file as part of a lending decision, and it can shave a few points off your score. A soft inquiry is a lower-stakes check that does not affect your score. Because SALT does not access your credit file for the lending decision at all, applying creates no inquiry of either kind. You can apply, get a quote, and even decide not to proceed without leaving a footprint on your credit report.

Note that no credit check does not mean no verification. SALT still performs standard identity verification (KYC) and anti-money-laundering screening, which are regulatory requirements. Those checks confirm who you are; they do not evaluate your creditworthiness and they do not touch your credit file.

Do Bitcoin-Backed Loans Show Up on Your Credit Report?

Generally, no. Crypto-backed lenders are typically not furnishers of data to the major consumer credit bureaus (Equifax, Experian, and TransUnion), so the loan usually does not appear on your credit report, does not add to your reported debt load, and does not change your credit utilization or debt-to-income calculations that other lenders see.

This cuts both ways, and it is worth being honest about the trade-off:

- The upside: borrowing does not increase your visible debt burden. If you are preparing to apply for a mortgage, for example, a Bitcoin-backed loan generally will not show up in the debt-to-income math the way a personal loan or HELOC would, though mortgage underwriters may still ask about large deposits or other obligations.

- The downside: on-time payments typically will not help you build or repair credit, because the positive payment history is not being reported either. If credit building is your goal, this is not the tool for it.

Reporting practices can vary by lender and can change, so if this detail is important to your planning, confirm it with your lender before signing.

What Happens to Your Credit If the Loan Goes Wrong?

With an unsecured loan, missing payments leads to late marks, collections, and potentially a charge-off on your credit report, damage that can follow you for years. A Bitcoin-backed loan resolves differently. If your collateral falls in value or payments stop, the outcome is handled through the collateral itself, typically a margin call and, if unresolved, liquidation of some or all of the pledged crypto.

Losing collateral to liquidation is a real financial loss and should be taken seriously, but it is generally a contained one: it does not ordinarily generate the cascade of credit-report damage that defaulting on unsecured debt does. SALT also offers tools designed to reduce liquidation risk in the first place, including SALT Shield® and Stabilization, which help qualifying borrowers manage volatility without losing their position.

Can a Bitcoin-Backed Loan Indirectly Improve Your Credit?

Indirectly, yes, depending on how you use the funds. A common strategy is using a Bitcoin-backed loan to consolidate or pay down high-interest credit card balances. Paying down revolving balances lowers your credit utilization ratio, one of the biggest factors in your score, while the new loan itself stays off your report. Borrowers effectively swap reported, high-interest revolving debt for unreported, collateral-secured debt.

Whether that trade makes sense depends on your rates, your risk tolerance around crypto volatility, and your discipline in repaying the new loan. It is a strategy worth discussing with a financial advisor rather than a guaranteed win.

Bitcoin-Backed Loans vs. Traditional Credit Products

Here is how the credit mechanics compare at a glance:

- Personal loan: hard inquiry at application, appears on your credit report, on-time payments build credit, default damages your score.

- Credit card: hard inquiry, ongoing utilization reporting, high rates on carried balances.

- HELOC: hard inquiry, credit reporting, plus a lien on your home and weeks of underwriting.

- Bitcoin-backed loan: no credit check, no hard inquiry, typically no credit reporting in either direction, secured by your crypto, with funding from SALT in as little as 24 to 48 hours after signing.

For a deeper comparison of costs and structures, see our guide to Bitcoin-backed loans vs. HELOCs and personal loans.

Frequently Asked Questions

Do crypto loans affect your credit score?

Applying for a crypto-backed loan from a lender like SALT does not affect your credit score, because there is no credit check and no hard inquiry. The loan is secured by your digital assets, and it typically is not reported to consumer credit bureaus, so it generally has no direct effect on your score in either direction.

Can I get a Bitcoin-backed loan with bad credit?

Yes. Because underwriting is based on your collateral rather than your credit history, borrowers with poor credit, thin credit files, or no U.S. credit history can qualify. What matters is the value of the crypto you pledge and the loan-to-value ratio you select.

Does SALT do a hard credit pull when I apply?

No. SALT does not perform a credit check of any kind, hard or soft, as part of its lending decision. Identity verification (KYC) is still required, but it does not involve your credit file.

Will my Bitcoin-backed loan show up when I apply for a mortgage?

It generally will not appear on your credit report, since crypto-backed loans are typically not reported to the bureaus. However, mortgage underwriters may ask you to disclose obligations and explain large deposits, so be prepared to document the loan honestly during a mortgage application.

Can a Bitcoin-backed loan help me build credit?

Usually not. Because payments are typically not reported to credit bureaus, on-time payments will not add positive history to your credit file. If building credit is your primary goal, a credit-builder loan or secured credit card is better suited to that job.

What do Bitcoin-backed lenders check instead of credit?

Lenders like SALT verify your identity, screen for compliance requirements, and evaluate your collateral: the type of digital asset, its value, and the LTV you choose. Loan terms at SALT run from 12 to 60 months with LTVs up to 70%, and approval does not depend on income documentation or credit history.

The Bottom Line

Bitcoin-backed loans occupy a unique spot in your financial toolkit: they let you access liquidity without a credit check, without a hard inquiry, and typically without any trace on your credit report, all while keeping your long-term crypto position intact. The trade-off is that they will not build your credit, and the real risk lives in collateral volatility rather than credit damage. If that fits your situation, you can get started in minutes. Sign up for a SALT account or explore current terms on our Rates & Fees page.

Disclaimers

Loan availability varies by jurisdiction. SALT loans are currently available throughout the United States and in select international jurisdictions, including Canada, Puerto Rico, Brazil, Portugal, Switzerland, the United Kingdom, the United Arab Emirates, Vietnam, Australia, New Zealand, and the Northern Mariana Islands. For the complete and current list of eligible jurisdictions, visit saltlending.com/map-list. Loan terms may vary or may not be available in your jurisdiction, for your requested loan amount, and/or preferred collateral type. Rates and terms are subject to change.

This content is for informational purposes only and does not constitute financial, investment, tax, legal, or credit advice. Credit scoring and credit reporting practices vary and may change; consult your lender and a qualified financial or credit professional regarding your specific circumstances. Borrowing against collateral entails risk and may not be appropriate for your needs. Digital currency is not legal tender, is not backed by the United States or any other government, and SALT accounts are not subject to FDIC or SIPC protections.