Important Notice

The term “Supplemental Income Strategy” describes a method for supplementing your liquidity by accessing cash from your bitcoin holdings through a loan. It does not imply that loan proceeds are income. Loan proceeds are debt, and borrowing against collateral entails risk. The information contained herein is for informational purposes only and does not constitute investment, financial, tax, or other professional advice. Loan availability, rates, and product features vary by jurisdiction and are subject to change.

Key Takeaways

- Long-term bitcoin holders can access cash without selling by borrowing against their bitcoin.

- SALT’s Supplemental Income Strategy combines Financed Interest (no monthly payments during the loan term) with SALT Shield™ (forbearance of margin call enforcement for the loan term, subject to conditions).

- The structure is designed to be repeatable through annual refinance cycles, providing ongoing liquidity access while the bitcoin position remains intact.

- Loan proceeds are debt, not income. Borrowing against collateral involves risk, including potential loss of collateral.

- The effectiveness of the structure depends on starting LTV and loan structure, not market timing.

Bitcoin holders tend to reach a point where the question changes. At first, the focus is accumulation. Then it becomes security. Over time, as conviction builds and holdings grow, a more practical question emerges: how do you actually use bitcoin without selling it?

For many long-term holders, the options can feel limited. Selling converts bitcoin into cash but may trigger a taxable event and reduce future upside. Holding preserves the asset but keeps its value locked up.

There is another approach.

SALT’s Supplemental Income Strategy is designed to provide predictable access to liquidity by borrowing against bitcoin rather than selling it. Built on two core components—Financed Interest and SALT Shield™—the structure allows borrowers to access cash, maintain their bitcoin position, defer payment obligations during the loan term, and forbear margin call enforcement for the loan term, subject to required conditions.

Loan proceeds are debt, not income. This structure is intended to supplement liquidity, not replace earned income.

Why Borrow Against Bitcoin Instead of Selling?

Selling bitcoin is simple, but it comes with tradeoffs.

Once sold, the asset is gone. Any future appreciation no longer benefits the seller. In addition, selling appreciated bitcoin may trigger capital gains, which can be significant depending on cost basis and jurisdiction.

Borrowing against bitcoin offers a different path.

Instead of selling, bitcoin is pledged as collateral in exchange for a loan. The borrower receives funds while retaining ownership of the underlying asset. Because ownership is retained when bitcoin is pledged as collateral, borrowing against bitcoin is generally not treated as a sale in many jurisdictions—though tax treatment varies, and borrowers should consult a qualified tax advisor regarding their specific situation.

For long-term holders, this creates a way to access cash while keeping their bitcoin position intact.

How to Get Cash From Bitcoin Without Selling

At a high level, the process is straightforward.

A borrower deposits bitcoin as collateral, selects a loan amount based on a chosen loan-to-value (LTV) ratio, and receives loan proceeds in USD. The bitcoin remains pledged to the loan rather than being sold.

Where SALT’s approach differs is in how the loan is structured.

Rather than relying on a standard bitcoin-backed loan with monthly payments and ongoing margin call risk, SALT’s Supplemental Income Strategy combines two features:

- Financed Interest — no monthly payments during the loan term.

- SALT Shield™ — forbearance of margin calls and market-triggered liquidation for the loan term, provided the borrower remains current on any required loan payments and subject to the Shield Terms and Conditions.

Together, these features allow the loan to function as a repeatable liquidity structure rather than a one-time borrowing event.

The Core Structure

The structure is designed to be simple and repeatable.

A borrower originates or refinances a loan at a conservative LTV, elects Financed Interest so there are no monthly payments during the term, and enrolls in SALT Shield™ once eligible. Loan proceeds are received upfront. At maturity, the loan is designed to be refinanced—settling deferred interest and drawing new proceeds for the next cycle.

This creates a framework for ongoing liquidity access while the underlying bitcoin position remains pledged but intact.

What Is Financed Interest?

Financed Interest is a SALT loan feature that capitalizes interest at origination and defers payment obligations until maturity or refinance.

This means:

- No monthly payments are required during the loan term.

- Interest is added to the loan balance upfront.

- Payment is settled at maturity or upon refinance.

This structure changes how the loan behaves. Instead of requiring ongoing payments, the borrower receives proceeds today and defers repayment obligations—allowing the liquidity accessed to remain available rather than being used for monthly servicing.

Jurisdictional Availability

Financed Interest is only available in jurisdictions where balloon payment loan structures are permitted. Borrowers should confirm availability before applying. For the most current list of supported jurisdictions, visit saltlending.com/map-list.

What Is SALT Shield™?

SALT Shield™ is SALT’s no-liquidation loan upgrade.

For a one-time fee, SALT agrees to forbear margin calls and market-triggered liquidation for the remainder of the loan term, subject to the loan agreement and Shield Terms and Conditions, provided the borrower remains current on any required loan payments.

This is a key distinction from standard crypto lending models. In traditional structures, falling bitcoin prices can trigger margin calls, requiring borrowers to add collateral or repay part of the loan. If no action is taken, forced liquidation may occur. SALT Shield™ is designed to remove that dynamic for the duration of Shield coverage.

Key considerations include:

- Available on eligible loans, typically $50,000+.

- LTV must be below 70% at enrollment.

- Must be added at least 3 months before maturity.

- Collateral withdrawals are not permitted while enrolled.

- If the loan is refinanced, re-enrollment is required.

- Available on 12-month loans.

See the SALT Shield™ Terms and Conditions for complete details, eligibility, pricing, and jurisdictional restrictions.

How the Annual Liquidity Cycle Works

The structure is intended to operate on a repeatable cycle, typically aligned with annual loan terms:

1. Originate or refinance a loan at a conservative LTV (typically 30–50%).

2. Elect Financed Interest so no monthly payments are required during the term.

3.Receive loan proceeds as a single upfront disbursement.

4. Enroll in SALT Shield™ once eligible.

5. At maturity, refinance the loan —settling deferred interest and drawing new proceeds.

6. Re-enroll in SALT Shield™ on the new loan to maintain forbearance coverage.

7. Repeat the cycle as long as the structure continues to fit your liquidity needs and risk tolerance.

The objective is to provide ongoing access to liquidity without requiring the sale of bitcoin—while making clear that each cycle is a new loan, with its own terms, eligibility, and risks.

Illustrative Example

The example below uses a bitcoin price of $80,000 and a collateral position of 5 BTC (total value $400,000). Figures are illustrative only and do not represent actual loan terms, available rates, or outcomes. Net cash figures will depend on the current Financed Interest rate, loan term, and applicable fees.

| Starting LTV | Loan Amount | Net Cash to Borrower | Profile |

|---|---|---|---|

| 30% | $120,000 | Loan amount less financed interest | Most conservative; largest buffer |

| 50% | $200,000 | Loan amount less financed interest | Balanced liquidity and buffer |

In each scenario, no monthly payments are required during the loan term, interest is financed and deferred, and loans may be eligible for SALT Shield™ once the eligibility criteria are met.

Actual rates, available LTVs, terms, and outcomes vary based on loan size, term length, eligibility, market conditions, and jurisdiction. Quoted rates and fees apply at origination and may change for subsequent refinances.

Why Starting LTV Matters

The most important decision in this structure is where you start.

A lower starting LTV provides:

- A larger buffer against bitcoin price declines.

- Greater flexibility at refinance.

- Lower SALT Shield™ fees (generally).

- A more sustainable structure over multiple cycles.

SALT supports LTVs up to 70%, though for this structure we typically recommend 30–50%, depending on liquidity needs and risk tolerance.

Who This Strategy Is Designed For

This structure is best suited for:

- Long-term bitcoin holders who want access to cash without selling.

- Individuals seeking recurring access to liquidity from a non-traditional asset.

- Borrowers looking to avoid an immediate taxable sale of appreciated bitcoin.

- Those who want to forbear margin call enforcement during the loan term via SALT Shield™.

It is not designed for short-term borrowing with a defined repayment event. In those cases, a standard loan structure may be more appropriate.

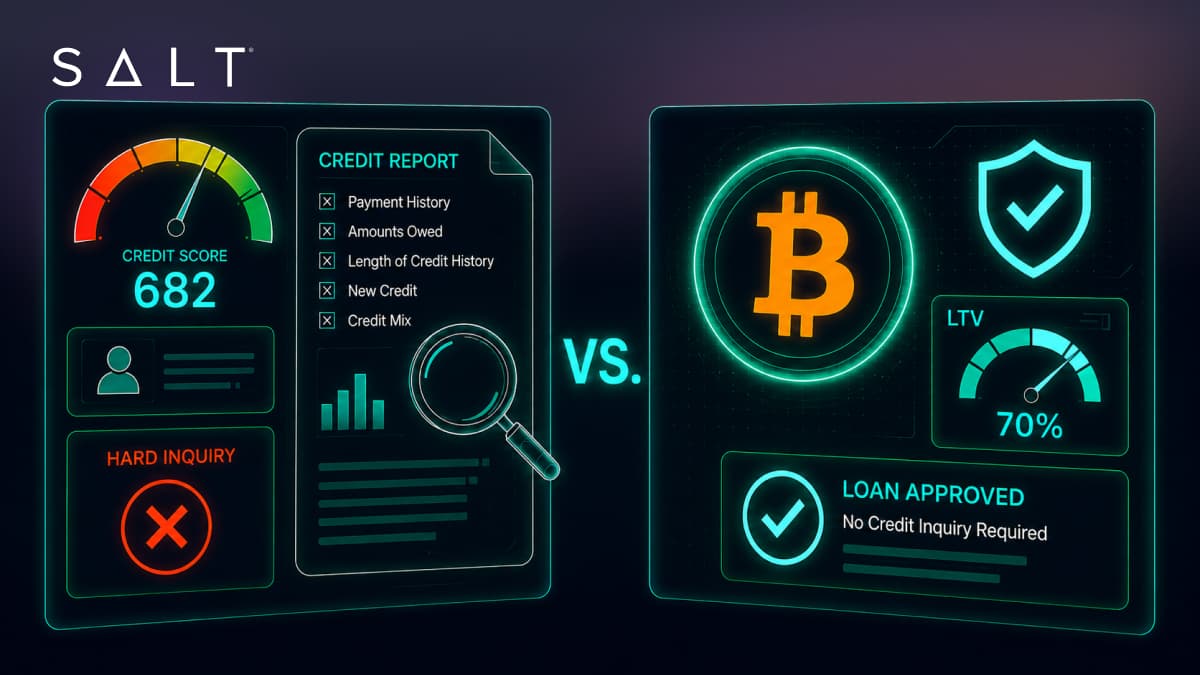

How This Compares to Other Liquidity Options

Bitcoin holders generally have several options for accessing capital. Each serves a different purpose:

| Sell Bitcoin | HELOC / Traditional | Standard Crypto Loan | Supplemental Liquidity Strategy |

|---|---|---|---|

| Immediate liquidity | Requires real estate or other collateral | Liquidity without selling | Liquidity without selling |

| Ends bitcoin exposure | Credit-based underwriting | Monthly interest payments | No monthly payments during the loan term (with Financed Interest) |

| May trigger capital gains | Closing costs, appraisals | Margin call and liquidation risk | Margin call enforcement waived with SALT Shield™ (subject to conditions) |

| One-time transaction | One-time loan with amortization | One-time disbursement | Structured for annual refinance cycles |

This structure is specifically designed for long-term holders seeking repeatable liquidity access.

What Happens if Bitcoin’s Price Changes?

If bitcoin increases in value, the borrower’s LTV decreases, potentially creating more borrowing capacity at refinance.

If bitcoin declines and SALT Shield™ is active, the price drop does not trigger a margin call or forced liquidation during the loan term, subject to the Shield Terms. At maturity, if LTV is elevated, the borrower must address it through repayment or collateral adjustment before refinancing.

For a deeper look at how LTV moves with the market, see how volatility thresholds work in bitcoin-backed lending.

Turning Bitcoin From a Static Holding Into a Usable Financial Asset

Many bitcoin holders want to use their bitcoin without selling it. Far fewer have a structure that allows them to do so in a consistent and controlled way.

SALT’s approach is designed to help long-term holders treat bitcoin as a usable financial asset on the balance sheet—one that can support ongoing liquidity needs while remaining pledged but intact.

Getting Started

To implement this structure:

1. Apply for a SALT loan at saltlending.com.

2. Select your loan amount and LTV —a lower starting LTV generally provides more flexibility.

3. Elect Financed Interest and confirm availability in your jurisdiction.

4. Add SALT Shield™ once your loan is funded and you meet eligibility requirements.

5. Receive proceeds and plan your annual refinance cadence.

→ SCHEDULE A CALL WITH OUR TEAM

Questions? Contact our team at [email protected] or call 1-800-931-1259 (Monday–Friday, 9AM–5PM MST).

Related reading: Volatility Thresholds in Bitcoin-Backed Lending • Borrow Against Bitcoin vs. Sell

Frequently Asked Questions

How can I get cash from bitcoin without selling it?

By borrowing against it. With SALT, bitcoin is used as collateral to access loan proceeds while you retain ownership of the asset.

Can I get a bitcoin loan with no monthly payments?

Yes, with Financed Interest. Interest is capitalized at origination and deferred until maturity or refinance. Availability depends on jurisdiction—specifically, whether balloon payment loan structures are permitted.

What is SALT Shield™?

SALT Shield™ is a no-liquidation loan upgrade that forbears margin calls and market-triggered liquidation for eligible loans during the duration of the loan, provided required conditions are met. It is a contractual forbearance—not an insurance product.

What LTV should I start with?

SALT supports 30–70% LTV, but for this structure we typically recommend 30–50% depending on risk tolerance and liquidity needs. Lower LTVs provide more buffer and flexibility.

Are loan proceeds taxable?

Loan proceeds are debt, not income, and are generally not treated as a sale of the underlying collateral in many jurisdictions. Tax treatment varies based on individual circumstance and applicable law. Consult a qualified tax advisor.

Is there a credit check?

No. SALT loans are collateral-based and do not require a credit check.

Is the “Supplemental Income Strategy” an income product?

No. The term “Supplemental Income Strategy” describes a method for supplementing your liquidity by accessing cash from your bitcoin through a loan. It does not imply that loan proceeds are income. Loan proceeds are debt.

What happens when the loan matures?

At maturity, you can repay the loan in full (including capitalized interest) or refinance into a new loan. Refinancing into a new term restarts the structure and requires re-enrollment in SALT Shield™ if you want continued forbearance coverage.

Who do I contact if I have questions?

Loan Support: [email protected] | 1-800-931-1259. Sales Team: [email protected] | Schedule a call at saltlending.com. Office hours are Monday–Friday, 9AM–5PM MST.

Important Disclosures

SALT Lending LLC (NMLS #1711910). This content is for informational and educational purposes only and does not constitute financial, investment, tax, accounting, or legal advice, nor a recommendation to buy, sell, hold, or borrow against any asset. The term “Supplemental Income Strategy” describes a structure for accessing liquidity through borrowing; it does not imply that loan proceeds are income. Loan proceeds are debt.

Borrowing against bitcoin involves risk, including market volatility, margin call events, and the potential loss of collateral. All illustrative examples are hypothetical and do not represent actual loan terms, available rates, or outcomes. Net cash figures will depend on the current Financed Interest rate, loan term, and applicable fees. Past performance and historical market behavior are not indicative of future results.

Financed Interest is available only in jurisdictions where balloon payment loan structures are permitted. SALT Shield™ is subject to eligibility requirements, pricing, and jurisdictional restrictions that may change from time to time at SALT’s discretion; see the SALT Shield™ Terms and Conditions for complete details. SALT Shield™ is a contractual forbearance of SALT’s margin call rights for the Shield coverage period—it is not an insurance product. Payment obligations on interest and principal are unchanged, and the full loan balance is due at maturity regardless of LTV at that time.

Loan products, eligibility requirements, LTV options, interest rates, fees, durations, and terms are subject to change and are governed by the loan agreement. Each refinance is a new loan with its own terms, eligibility, and pricing. Refinancing and the conversion or sale of pledged collateral may have tax consequences depending on your jurisdiction; consult a qualified tax advisor.

SALT products and services are not available in all jurisdictions. For the most current list of supported jurisdictions, please visit saltlending.com/map-list.