Key Takeaway

Volatility thresholds are LTV-based signals — not liquidation triggers. They create time for borrowers to act by adding collateral, paying down principal, or adjusting strategy. Stabilization preserves collateral value by converting to USDC instead of liquidating, and SALT Shield™ can remove margin call risk entirely for eligible loans.

Bitcoin does not move in straight lines. It trends, corrects, rallies, and sometimes drops with speed that traditional markets rarely experience. For long-term holders, that volatility is part of bitcoin’s character. But when bitcoin is used as collateral in a secured loan, volatility becomes more than a market feature—it becomes a structural input inside the loan itself.

Understanding volatility thresholds is therefore not optional. It is foundational to borrowing responsibly against bitcoin.

At SALT Lending, bitcoin-backed loans are designed around visibility and risk alignment. Loan-to-value (LTV) tiers, continuous monitoring, loan health alerts, Stabilization, and SALT Shield™ all exist to manage how price movement interacts with loan health in real conditions—not theoretical ones.

This guide explains how volatility thresholds actually work, how they relate to LTV and pricing, and how borrowers can design strategies around volatility rather than react to it.

Volatility Is the Variable. LTV Is the Control.

When you take out a bitcoin-backed loan, you enter a secured lending structure. Your BTC serves as collateral, and the lender extends capital based on its value.

The central measurement governing this relationship is Loan-to-Value (LTV):

LTV = Loan Amount ÷ Collateral Value

If you borrow $50,000 against $100,000 worth of BTC, your LTV is 50%.

That single percentage quietly governs almost everything about your loan. It determines your buffer against price movement, your interest-rate tier, and how quickly market volatility affects your position.

Crucially, LTV is not fixed. It changes as bitcoin’s price changes. When BTC rises, collateral value increases and LTV falls. When BTC declines, collateral value falls and LTV rises.

Volatility thresholds are predefined LTV markers that signal when this shifting balance has moved into a higher-risk zone. They are not surprises or penalties. They are structured signals designed to create time and optionality.

Why Loan-to-Value Tiers Exist

Not all borrowers have the same goals. Some prioritize maximum liquidity. Others prioritize long-term stability. LTV tiers exist to reflect those different priorities.

SALT typically offers multiple LTV options—each representing a different balance between liquidity and collateral buffer:

- A lower LTV structure provides a wider cushion against price declines, typically comes with lower interest rates, and often allows for longer loan terms.

- A mid-range LTV balances liquidity with moderate exposure to volatility.

- A higher LTV provides more capital upfront but leaves less buffer, increases sensitivity to price swings, and is priced accordingly.

According to SALT’s published Rates and Fees, interest rates generally increase as LTV increases. This is intentional. The more you borrow relative to your collateral, the more exposed your position becomes to market movement—and pricing reflects that exposure. This is not a penalty model. It is risk alignment by design.

Current LTV options and rates are subject to change. Review your available tiers at saltlending.com or within your account dashboard.

What Actually Happens When Bitcoin Moves

To understand volatility thresholds in practice, consider a simple scenario.

You open a loan at 50% LTV when bitcoin is priced at $100,000. You borrow $50,000 against one BTC.

If bitcoin drops to $80,000, your loan balance stays the same, but your collateral value falls. Your LTV rises to 62.5%. You did not borrow more money—the market moved beneath you.

As bitcoin continues to move, your LTV adjusts automatically. When it approaches predefined thresholds, alerts are triggered. This does not automatically mean liquidation. It means visibility.

The system is designed to notify you before a situation becomes critical, giving you the opportunity to respond while options are still available.

Monitoring Turns Volatility Into Visibility

Volatility becomes dangerous when it is invisible. SALT’s monitoring infrastructure continuously tracks collateral value, loan balance, and real-time LTV.

Borrowers can configure loan health notifications via email, SMS, phone, or push notifications. If LTV begins rising toward a threshold, you are informed early—even during fast-moving markets.

That visibility gives you control. You can add collateral, reduce outstanding principal, or adjust strategy before risk escalates. This is proactive collateral management, not reactive panic.

Volatility Thresholds Are Not Liquidation Triggers

A common misconception is that crossing a volatility threshold automatically results in liquidation. In reality, thresholds function as stages in a structured risk ladder:

- At elevated LTV levels, loan health alerts are issued so you have time to act.

- At the Margin Call LTV, a formal margin call is issued, recommending that you add collateral or pay down principal.

- At the Stabilization LTV (90.91%), SALT Stabilization, when enabled, engages automatically—converting your collateral to USDC in lieu of liquidation to help preserve value.

The earlier a borrower responds, the more optionality they preserve. Volatility thresholds exist to create time, not remove it. Consequences defined in your loan agreement—which may ultimately include the sale of collateral—apply if LTV is not restored in accordance with your loan terms.

Pricing and Risk Move Together

Lower-LTV loans typically carry lower rates because they have more collateral buffer. Higher-LTV loans carry higher rates because they are more sensitive to price movement.

This structure ensures that borrowers choosing higher liquidity accept higher exposure, while borrowers prioritizing stability benefit from more conservative pricing. Understanding this trade-off is essential. The decision is not simply about rate—it is about volatility tolerance.

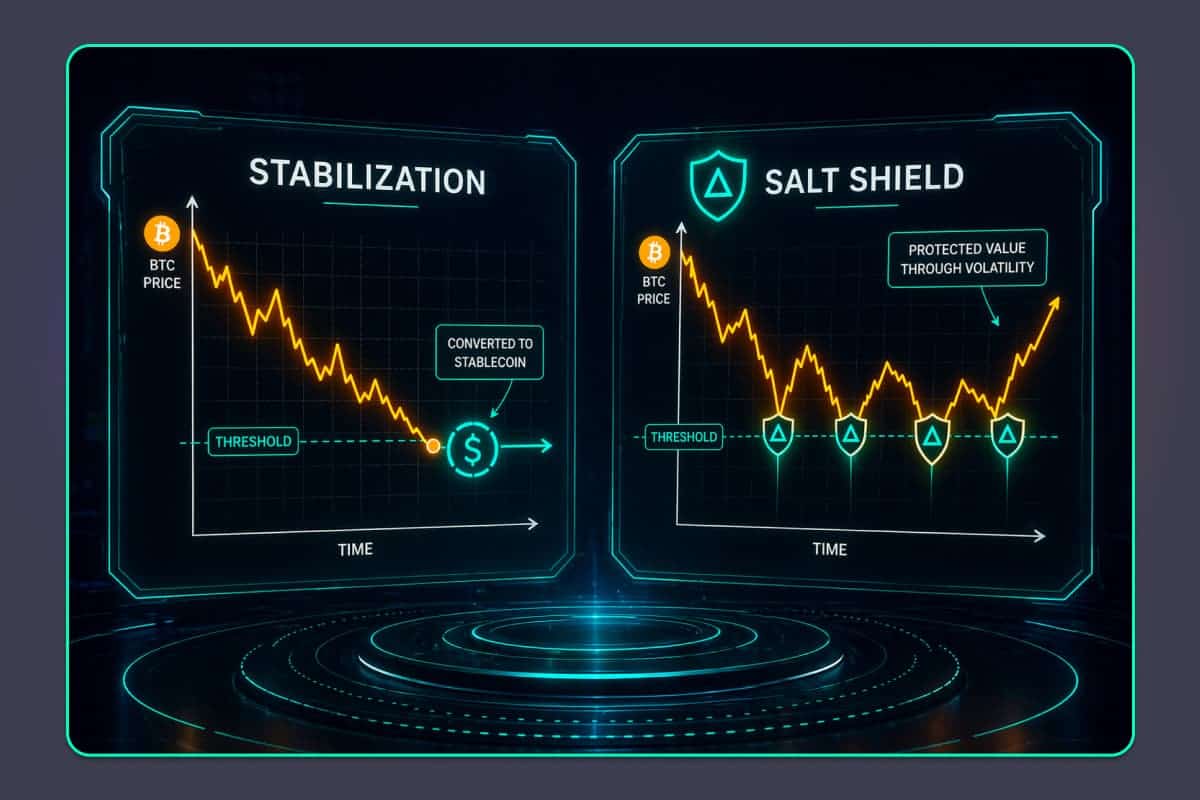

Stabilization: Value Preservation in Lieu of Liquidation

Stabilization is a core feature of the SALT loan—not a separate product. It is the mechanism that engages when a loan reaches the Stabilization LTV threshold of 90.91%.

At that point, rather than liquidating your BTC collateral outright, SALT automatically converts it to USDC (a US-dollar stablecoin), powered by STAMP™, SALT’s proprietary execution engine. The practical effect is that the dollar value of your collateral is locked in at the moment of conversion, rather than being sold into a falling market at open-market prices.

After Stabilization engages, you’re not stuck in USDC permanently. You can restore loan health and re-enter your original crypto position by:

- Depositing additional collateral, or

- Making a principal payment

Once your LTV is returned below 83.33%, you’re eligible to convert the USDC back into BTC (or your original collateral mix), subject to then-current market prices and applicable transaction fees.

Stabilization does not guarantee you’ll convert back at a favorable price. What it does is give you breathing room: instead of your position being sold off at a volatility low, the value is held in a stable asset while you decide the next move.

You can review the full mechanics on the Stabilization page.

SALT Shield™: The No-Liquidation Solution

For borrowers who want to remove margin call risk from the equation entirely, SALT offers a loan upgrade called SALT Shield™.

SALT Shield™ is a one-time-fee upgrade in which SALT agrees to forbear enforcement of its margin call rights for the duration of the loan. In practical terms: if you’re enrolled in SALT Shield and keeping up with your loan payments, short-term price drops will not trigger margin calls or forced conversions against your BTC collateral.

A few things to know:

- One-time fee. Pricing is shown before you commit. Lower-LTV loans generally carry lower Shield fees.

- Eligibility requirements apply. At the time of this writing, Shield is available for active loans above a minimum loan size, with LTV below 70%, and more than three months from maturity. Availability, pricing, and terms are subject to change and jurisdictional restrictions. SALT Shield is currently included on eligible 1-year loans at 30% LTV.

- No collateral withdrawals. Once Shield is purchased, no collateral may be withdrawn until the loan’s maturity date, regardless of LTV.

Eligibility, pricing, and full terms are published in the SALT Shield™ Terms and Conditions.

Stabilization and SALT Shield™: How They Compare

It helps to think of Stabilization and SALT Shield as two layers operating at different points on the risk ladder:

- Stabilization is built into the SALT loan if selected. It engages at 90.91% LTV and preserves collateral value by converting BTC to USDC rather than liquidating at market.

- SALT Shield™ is an optional upgrade on eligible loans. It forbears margin call and Stabilization enforcement entirely for the loan term—meaning short-term price drops won’t trigger a conversion out of BTC in the first place.

For borrowers who prioritize staying in BTC through volatility, Shield changes the equation. For borrowers who don’t carry Shield, Stabilization still provides a value-preserving alternative to outright liquidation.

How Volatility Intersects With Refinancing

Volatility does not operate in isolation. It directly affects refinancing opportunities.

When bitcoin appreciates significantly, LTV falls. That lower LTV may create opportunities to refinance, adjust loan terms, or access additional liquidity. Conversely, if volatility increases risk exposure, refinancing into a lower-LTV structure can reduce sensitivity to price swings and support more predictable liquidity planning.

Volatility thresholds, LTV tiers, Stabilization, SALT Shield eligibility, and refinancing decisions all sit within the same broader liquidity-planning framework.

Two Borrowers, Two Outcomes

Consider two borrowers facing the same market movement.

One chooses a conservative 30% LTV structure on a 1-year loan and opts in for SALT Shield. Bitcoin drops 25%. Their LTV rises, but Shield forbears margin call enforcement—no action is required, and their BTC collateral remains intact.

Another chooses a 70% LTV structure without Shield. The same price drop pushes LTV sharply higher, triggering alerts and eventually the margin call process. If LTV isn’t restored and continues to climb, Stabilization will engage at 90.91% LTV, converting their collateral to USDC to preserve dollar value.

Neither approach is inherently wrong. Each reflects different priorities. Understanding volatility thresholds—and the tools that operate at each one—allows borrowers to choose intentionally rather than reactively.

Volatility as Strategy, Not Fear

Bitcoin’s volatility does not invalidate bitcoin-backed lending. It defines how it must be structured.

Effective loan design builds around price movement rather than assuming stability. LTV tiers establish your starting buffer. Volatility thresholds signal when risk is increasing. Monitoring and loan health alerts provide real-time visibility. Stabilization preserves collateral value in lieu of liquidation at the highest LTV threshold. And for eligible loans, SALT Shield can remove margin call risk from the picture altogether.

Together, these elements transform volatility from something chaotic into something measurable, manageable, and strategically integrated into the lending framework.

Frequently Asked Questions

What are volatility thresholds?

They are predefined LTV markers that signal increasing risk as bitcoin’s price changes. At SALT, key thresholds include margin call levels and the 90.91% Stabilization LTV.

Does reaching a threshold mean immediate liquidation?

No. Thresholds generally serve as warning stages that allow borrowers to act before more serious consequences occur. At 90.91% LTV, SALT’s Stabilization feature, when activated, converts collateral to USDC in lieu of liquidation, preserving dollar value.

Is a higher-LTV loan riskier?

Yes. Higher LTV means less collateral buffer and greater sensitivity to price swings.

Can I reduce my LTV after opening a loan?

Yes. Adding collateral or paying down principal lowers effective LTV and increases buffer.

How do SALT Shield™ and Stabilization differ?

Stabilization is an opt-in loan feature that engages at 90.91% LTV and converts your collateral to USDC in lieu of liquidation. SALT Shield™ is an optional loan upgrade, available on eligible loans for a one-time fee, in which SALT forbears margin call and Stabilization enforcement for the loan term—so short-term price drops don’t trigger a conversion out of BTC in the first place.

What happens after Stabilization converts my collateral to USDC?

You can restore loan health to below 83.33% LTV by depositing more collateral or making a principal payment, and then convert back to BTC (or your original collateral mix) subject to current market prices and transaction fees.

Review Your Loan Options Today

Create a SALT account to review your available LTV tiers, check SALT Shield™ eligibility, monitor your collateral health, and evaluate how your loan structure aligns with your volatility tolerance.

If you’re not yet a borrower, explore bitcoin-backed loan options and choose a structure that fits your liquidity strategy.

Important Disclosures

This content is for informational and educational purposes only and does not constitute financial, investment, tax, or legal advice. Borrowing against bitcoin involves risk, including the potential loss of collateral. Past performance and historical market behavior are not indicative of future results. The conversion or liquidation of pledged assets may result in tax consequences; please consult your tax advisor.

Loan products, LTV options, interest rates, fees, and terms are subject to change and are governed by your loan agreement. SALT Shield™ is subject to eligibility requirements, pricing, and jurisdictional restrictions that may change from time to time at SALT’s discretion; see the SALT Shield™ Terms and Conditions for complete details. SALT Shield™ is not an insurance product.

SALT products and services are not available in all jurisdictions. For the most current list of supported jurisdictions, please visit saltlending.com/map-list.