The following is for educational and informational purposes only. Content is not investment advice, nor an offer or solicitation to buy or sell any security of SALT or any other entity.

Bitcoin has changed the way individuals and institutions think about money. What began as an experiment is now a recognized global asset with long-term conviction behind it. Many holders are not speculators, they are long-horizon investors who treat Bitcoin like digital gold.

But long-horizon conviction comes with a practical dilemma:

What do you do when you need liquidity today, but you don’t want to sell your Bitcoin?

A Bitcoin-backed loan is the modern, tax-efficient, wealth-preserving answer.

This guide explains exactly how Bitcoin-backed loans work, why more holders now borrow instead of sell, how SALT Lending approaches the model, and what risks and opportunities you should understand before you take one.

In this guide, we’ll walk through everything you need to know:

- What bitcoin-backed loans are

- Why more bitcoiners are choosing to borrow instead of sell

- How bitcoin-backed loans work

- The risks you should understand

- When a BTC-backed loan is the right strategic move

- How SALT Lending fits into this picture

By the end, you’ll have a clear, practical understanding of why bitcoin-backed loans have become one of the smartest liquidity tools for long-term BTC holders.

1. What Is a Bitcoin-Backed Loan?

“What is a Bitcoin-backed loan?”

A Bitcoin-backed loan lets you borrow cash using your Bitcoin as collateral without needing to sell your BTC.

It mirrors a traditional secured loan:

- Homeowners borrow against property

- Stockholders borrow against portfolios

- Businesses borrow against assets

Bitcoin holders can borrow against their BTC in the same way, with the benefit of 24/7 collateral settlement, transparency, and global accessibility.

2. Why People Borrow Against Their Bitcoin Instead of Selling It

Reason #1: You avoid triggering a taxable event

When you sell Bitcoin, you realize capital gains but when you borrow against Bitcoin, you don’t. For many long-term holders, this is the single biggest reason to use a BTC-backed loan.

Reason #2: You preserve your long-term upside

Selling Bitcoin forces you to exit your position. Borrowing lets you keep your exposure while unlocking liquidity. If Bitcoin rises during the term of your loan, you keep the full benefit. This is why the strategy is often summarized in one sentence:

“Borrow, don’t sell.”

Reason #3: You get immediate access to cash

Borrowing against your Bitcoin gives you fast liquidity without needing to convert crypto to fiat. People use BTC-backed loans for:

- Buying a home

- Paying tax bills

- Funding a business

- Investing in real estate

- Consolidating high-interest debt

- Large purchases

- Emergency liquidity

Reason #4: You stay aligned with your investment thesis

HODL culture exists for a reason: Bitcoin is volatile short-term, but its long-term trajectory has historically been up. Borrowing lets you benefit from that while solving short-term liquidity needs.

Reason #5: It mirrors strategies the wealthy have used for decades

High-net-worth individuals and corporations have long used strategic borrowing:

- Borrowing against equities

- Borrowing against real estate

- Borrowing against business assets

Borrowing against Bitcoin is simply the modern equivalent.

3. How Bitcoin-Backed Loans Work (Step-By-Step)

Although the mechanics vary by lender, here is the general process, streamlined using SALT Lending as the model.

Step 1: Create an account and apply

You complete basic onboarding (ID verification, 2FA) and select your loan terms.

Step 2: Deposit your BTC collateral

Your Bitcoin is transferred into a secure, custody-protected wallet. This is your pledged collateral, you still own it, but it’s locked until repayment.

Step 3: Receive your loan funds

Once collateral is confirmed, you receive your loan payout to your chosen method:

- Bank account

- Stablecoin (depending on the platform)

Step 4: Make monthly payments

Your loan has:

- A fixed term (e.g., 12–60 months)

- A fixed interest rate

- A predictable repayment schedule

Step 5: Repay the loan and retrieve your BTC

Once your loan is fully repaid, your Bitcoin collateral is released back to you. No selling. No exit. No loss of upside.

4. Understanding Loan-to-Value (LTV) On Bitcoin Loans

The Loan-to-Value ratio determines how much you can borrow relative to the value of your Bitcoin.

For example:

- If you deposit $50,000 of BTC

- And take a loan at 30% LTV

- You could borrow $15,000

A lower LTV means:

- Less risk of margin calls

- More stability during volatility

SALT Lending offers multiple LTV options allowing borrowers to match their loan with their risk profile.

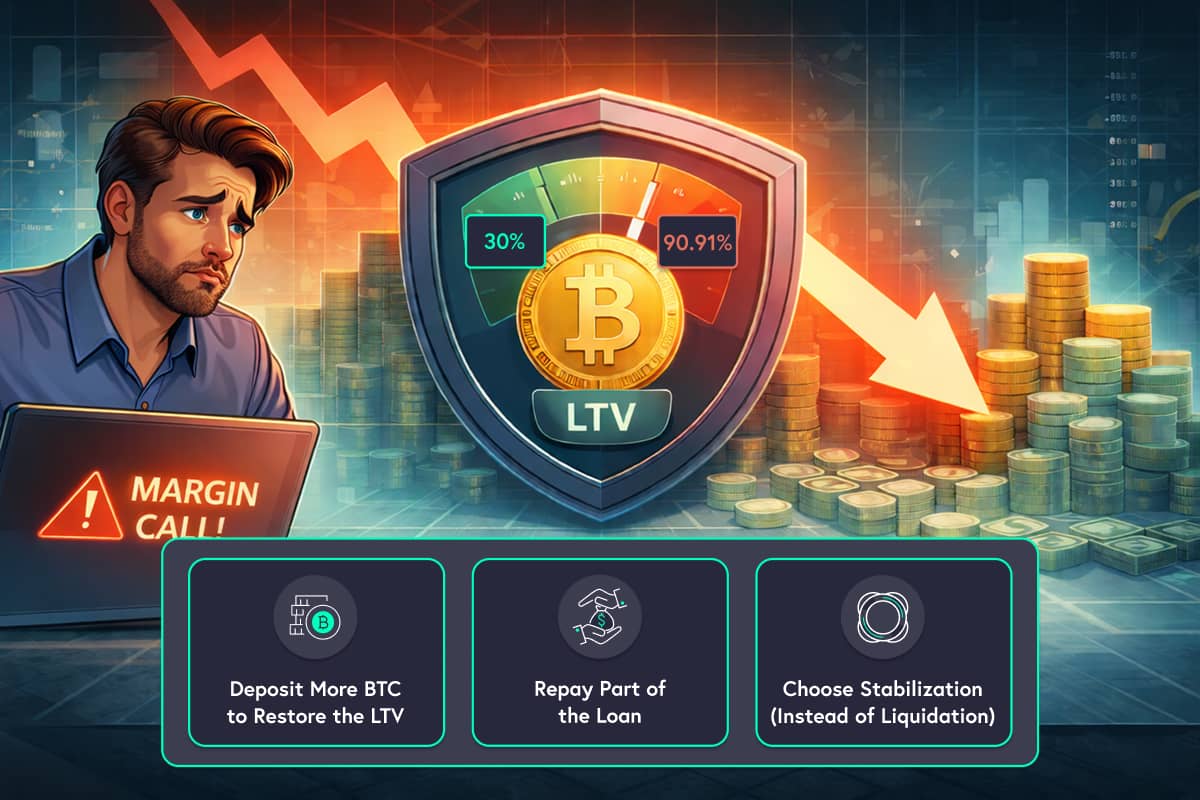

5. What Happens If Bitcoin’s Price Falls? (Margin Calls Explained)

Because BTC is volatile, lenders need a way to maintain collateral value. If Bitcoin’s price drops significantly, your collateral may no longer be sufficient to support the loan. This triggers a margin call.

With SALT, borrowers have options:

Option 1: Deposit more BTC to restore the LTV

The most common, and usually the simplest.

Option 2: Repay part of the loan

Lower balance → lower LTV.

Option 3: Choose Stabilization (instead of Liquidation) setting

SALT offers a Stabilization option where BTC is automatically converted to USDC, locking in its value.

This is one of the features that separates SALT from traditional crypto lending models.

6. Benefits of a Bitcoin-Backed Loan

Let’s break down the strategic advantages in detail.

• Immediate liquidity without selling

Get cash today without exiting your position.

• Preserve your future upside

If BTC appreciates, your wealth continues growing while your loan is active.

• Typically no tax trigger

Borrowing is not a taxable event in most jurisdictions.

• Flexible use of funds

Use the cash for personal, professional, or investment-related expenses.

• Predictable repayment structure

Fixed rates. Fixed terms. No surprises.

• A smarter alternative to high-interest debt

A BTC-backed loan can be used to consolidate or replace more expensive borrowing.

• A long-term strategy used by sophisticated investors

Borrowing against appreciating assets is a proven wealth-building method.

7. Risks to Consider (And How SALT Mitigates Them)

Risk 1: Bitcoin price volatility

Price swings can cause margin calls.

Mitigation:

SALT’s conservative LTV options + Stabilization gives borrowers more protection. SALT Shield™ is SALT Lending’s no-liquidation loan upgrade. For a one-time fee, get no more margin calls and market-triggered liquidations, keeping your collateral safe even in a market downturn

Risk 2: Loss of collateral

If you cannot meet margin calls and have selected liquidation, some or all collateral may be sold to cure your LTV back to a healthy state.

Mitigation:

SALT gives borrowers multiple options to save their collateral before liquidation.

Risk 3: Interest obligations

You must repay according to schedule.

Mitigation:

SALT offers fixed, transparent rates, no hidden fees.

Risk 4: Counterparty risk

Not all lenders are equal.

Mitigation:

SALT has been operating since 2016, the first, longest-standing, and most compliance-focused Bitcoin lenders.

8. When a Bitcoin-Backed Loan Makes Sense

✓ You want to stay long on BTC

If your thesis is long-term appreciation, a BTC-backed loan lets you keep your exposure.

✓ You need cash but don’t want to sell

This is the classic BTC-holder dilemma: liquidity vs. conviction.

Borrowing removes the tradeoff.

✓ You want to avoid capital gains tax

Selling can create a tax liability.

Borrowing doesn’t (in most jurisdictions).

✓ You want to fund opportunities without selling your Bitcoin

Real estate, business investment, renovations, or other ventures.

✓ You want to consolidate high-interest debt

BTC-backed loans typically offer better rates than credit cards or high-risk loans.

✓ You want a more sophisticated wealth strategy

Borrowing against appreciating assets is a proven method of maintaining long-term financial leverage.

9. Why Borrowing Against Bitcoin Is Growing in Popularity

The trend is clear:

More long-term BTC holders now borrow, rather than sell, because it aligns with how other asset classes are treated. Real estate investors don’t sell their homes to free up capital. They borrow against them. Stock investors don’t liquidate their portfolios to make a purchase. They borrow on margin. Bitcoin deserves, and increasingly receives, the same treatment.

As BTC’s adoption deepens, more lenders recognize the asset as credible collateral. And platforms like SALT Lending have evolved this into a highly secure, transparent, borrower-friendly model.

10. Why BTC-Native Borrowers Choose SALT Lending

Here’s what differentiates SALT from other lenders:

• Longest-standing Bitcoin lender (since 2016)

Experience matters when handling collateral like BTC.

• No rehypothecation

Your Bitcoin is never lent out, reused, or gambled with.

• Multiple safeguards for volatility

Stabilization. Conservative LTVs. Transparent margin call mechanics.

• Fixed rates and predictable terms

No surprise adjustments.

• Multi-year loan products

1-year, 3-year, and 5-year offerings for long-term planning.

• Clear, trusted, compliance-first framework

Security and protection are built into every step.

• Borrower-first product philosophy

SALT designs its products around protecting collateral, not liquidating it.

Borrowers who prefer responsible, transparent lending choose SALT because it behaves differently from the “wild west” crypto lenders of the past.

11. Borrowing vs. Selling: The Wealth Impact Over Time

Here’s a simple illustration:

Scenario A: You sell 1 BTC at $60,000 to access cash.

- You owe capital gains tax.

- If BTC hits $120,000 later, you’ve lost that upside.

- Your total long-term position shrinks.

Scenario B: You borrow $20,000 against 1 BTC at 33% LTV.

- No taxable event.

- If BTC hits $120,000, your collateral value doubles.

- You repay your loan and reclaim your BTC, plus all the upside.

Borrowing doesn’t just give you liquidity. It protects your long-term wealth trajectory.

Bitcoin-Backed Loans Are a Smart Liquidity Tool

Bitcoin is one of the most powerful stores of value of the modern era. If you’re committed to holding it for the long term, selling it for short-term liquidity rarely makes strategic sense.

A Bitcoin-backed loan allows you to:

- Keep your Bitcoin

- Access cash quickly

- Avoid taxable events

- Retain long-term upside

- Borrow like high-net-worth individuals do

This is why BTC-backed lending has become a core financial strategy for long-term Bitcoin holders, and why platforms like SALT Lending have built secure, responsible products designed specifically for the BTC-native community.

If you’re looking for liquidity and want to preserve, not sacrifice, your Bitcoin position, a BTC-backed loan is one of the smartest tools available.